THE GHOST IN THE MACHINE : SIGMA ADVANCED SYSTEM

The Confidence Trick That Isn’t One Yet

In 1949, Volkswagen sold its first Beetle in the United States. The car was small, ugly by American standards, and produced by a country that America had been at war with thirteen years prior. Conventional wisdom said it had no business succeeding in a market that worshipped tail fins and V8 engines. The ad agency Doyle Dane Bernbach did something audacious: they wrote an ad that simply said, ‘Think Small.’ They leaned into the car’s oddity. They made the weakness the story.

The Beetle became one of the best-selling cars in American history.

Now consider a different kind of story. A story where the oddity is real, the transformation is genuine in ambition, and the market has already priced in the happy ending before a single engine has been tested.

That is the Sigma Advanced Systems story as it stands in 2026

Let me tell you what this company actually is, layered carefully, because the surface narrative and the forensic reality diverge in ways that matter enormously to your portfolio.

Sigma Advanced Systems Limited is what happens when three very different things collide at high velocity: a dormant listed IT shell called Megasoft that had essentially zero operating revenue, an unlisted Hyderabad-based embedded systems company that spent 30 years quietly supplying avionics and airborne hardware to India’s defence establishment, and a UK precision engineering group called Nasmyth that was rescued from near-bankruptcy by a private equity firm in 2022 and sold three years later to an Indian buyer. And few other acquisitions and partnerships that we will explore in later parts.

These entities have now been stitched together under one listed vehicle, rebranded with a commanding name, given a compelling narrative about India’s defense export ambitions, and watched by the market with the kind of enthusiasm that tends to precede either a remarkable success story or a painful lesson in the difference between what a company is doing and what a company is becoming.

But here is the thing about complex corporate transformations: the most dangerous moment is not before the market believes the story. It is after. It is the period when the narrative has been priced in, the announcements have been made, and all that remains is for reality to catch up or not.

The Missile and the Mystery

A scene that contains the entire thesis

Somewhere over the Bay of Bengal, at a classified date in the last several years, an Indian Air Force SU-30 MKI fighter fired an ASTRA air-to-air missile at a drone target flying 80 km away. The missile found the target. The target ceased to exist. In the press release issued by the Ministry of Defense, a list of contributing organisations appeared. DRDO. HAL. BEL. The usual names right.

Inside the missile’s guidance electronics, inside the specific circuit board governing how the seeker searched for and classified its target was work done by a company that did not appear in that press release. A company based in Hyderabad’s Hardware Park, that had been doing exactly this kind of work for thirty years. A company that, until very recently, was not listed on any stock exchange. A company that, even now, almost no analyst covering the Indian defense sector has properly examined.

The greatest mispricings in public markets are almost always stories the market has been telling about the wrong company.

The market has been telling a story about Megasoft a dead telecom software company that ran out of revenue around 2023 and spent its final years as a listed vehicle holding a minority stake in a Swiss company. Technically accurate. Entirely wrong. Because what happened in December 2025 was not just a rebrand. It was a revelation. A private defense electronics company with thirty years of deployed technology on India’s most sensitive weapons systems quietly used a dormant listed shell to go public, then moved with unusual speed to acquire a UK precision engineering firm with Rolls Royce and Boeing as clients, a Delhi-based company with European defense programme access, and the exclusive supply partnership for what is arguably the world’s most sophisticated autonomous counter-drone technology.

This article exists to tell that story properly. Not as a research report. Not as a collection of data points in a table. As the story it actually is: complicated, genuinely exciting, genuinely risky, and genuinely unlike anything else in the Indian equity market right now.

One Question: What Type of Business Is This at Its Core?

This sounds obvious. It is not. And getting it wrong is the single most expensive mistake investors make.

The intuitive answer is: a defense and aerospace company. After all, that is how it describes itself. That is the sector it has classified itself in. That is the story the market is telling.

The correct answer is more uncomfortable: This is a roll up in early execution.

Let’s be precise about what that means, because ‘rollup’ is a term that gets used casually and often strips away what is actually important about the classification.

A rollup is a business model where the primary growth mechanism is acquisition buying other companies and consolidating them under one corporate roof rather than organic development of products, customers, or markets. The investment thesis in a rollup is fundamentally different from the investment thesis in an organic compounder, and this distinction matters enormously for how you evaluate the business and what metrics you track.

The Rollup Framework: Why Classification Changes Everything

Munger talks about the importance of using the right mental models for each situation, which he calls ‘the latticework of mental models.’ The rollup framework is a specific mental model that changes nearly every analytical question you ask. In a rollup, the right questions are: (1) Is the acquirer paying the right price for assets? (2) Can they extract synergies that the previous owners could not? (3) Is the acquisition currency (stock or debt) sustainable? (4) What is the integration track record?

This is what Megasoft was. A listed shell. A clean vehicle for someone with ambition to use.

The ambition came from Sigma Advanced Systems Private Limited the unlisted Hyderabad company and its promoter group, Chintalapati Holdings. They used the NCLT-sanctioned merger (a perfectly legal and common mechanism) to bring their unlisted defence business into the public markets via reverse merger, with a 316:100 share swap ratio that handed them 46.31 percent of the new entity. They then used the newly listed vehicle to acquire Nasmyth Group in the UK, rebrand the whole enterprise as Sigma Advanced Systems Limited.

This is not a criticism. It is a description. Reverse mergers have created genuine value before. The question is always the same: what is the quality of the assets being brought together, and what is the management’s actual track record of making acquisitions work?

SECTION 01

The Ghost in the Machine

The standard narrative goes: ambitious promoter finds a listed shell, injects an aerospace story into it, watches the stock re-rate on defence sector enthusiasm. This is the narrative that explains 186% in twelve months as pure narrative arbitrage. But the story is worth looking at.

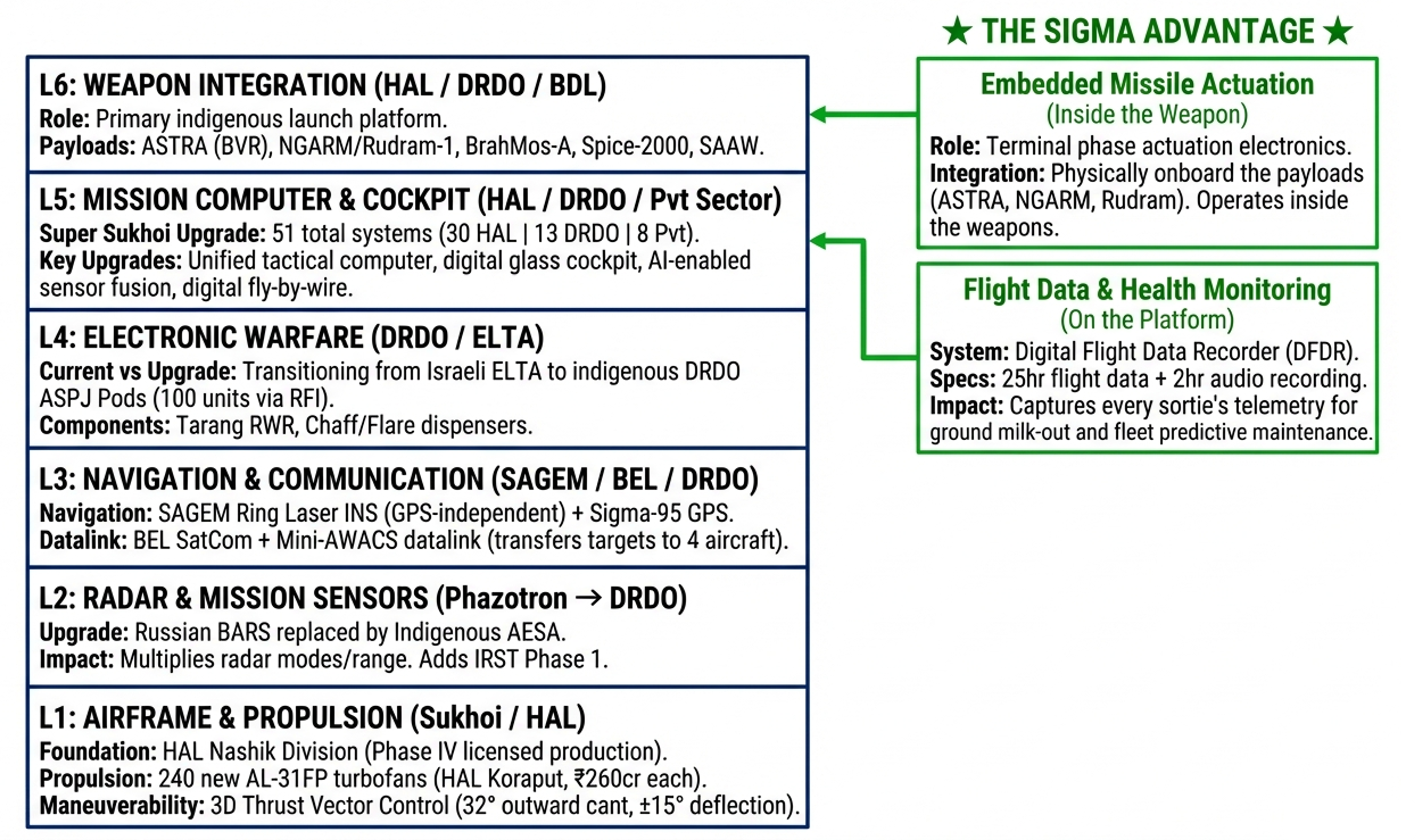

Sigma Advanced Systems Pvt Ltd. was not assembled to justify a stock re-rating that is lazy thinking. It was incorporated in 1994 three years before the Asian financial crisis, a decade before India’s defense modernisation became a serious policy priority by a Hyderabad engineer named Damodar Reddy. For three decades it did what the most valuable defense companies do: it made the things inside the things. Not the missile. The missile’s guidance electronics. Not the fighter jet. The fighter jet’s avionics suite.

What Sigma Has Actually Built?

Let us be specific. Because the investment thesis lives and dies in the specifics.

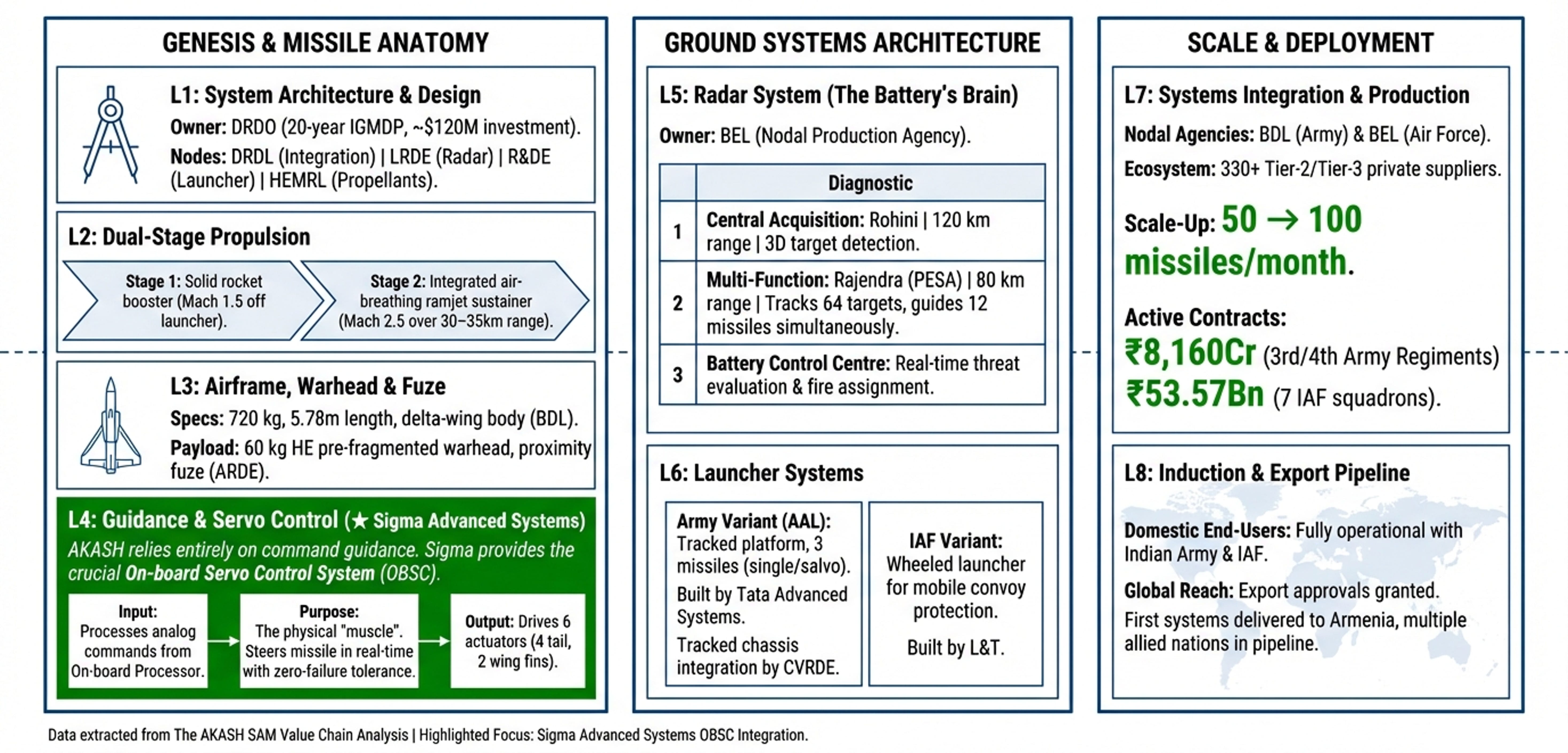

AKASH Surface-to-Air Missile. India’s primary medium-range air defense system, with eight-plus Indian Air Force squadrons operational and Army induction ongoing. The AKASH engages targets at up to 45 kms. Being on the AKASH supply chain requires a DGQA qualification (Directorate General of Quality Assurance). Sigma has been there. The successor programme, AKASH NG, extends the range to 80 kms and is in advanced development. Sigma’s existing qualification is the shortest path to AKASH NG electronics supply. Incumbency, in defense procurement, compounds.

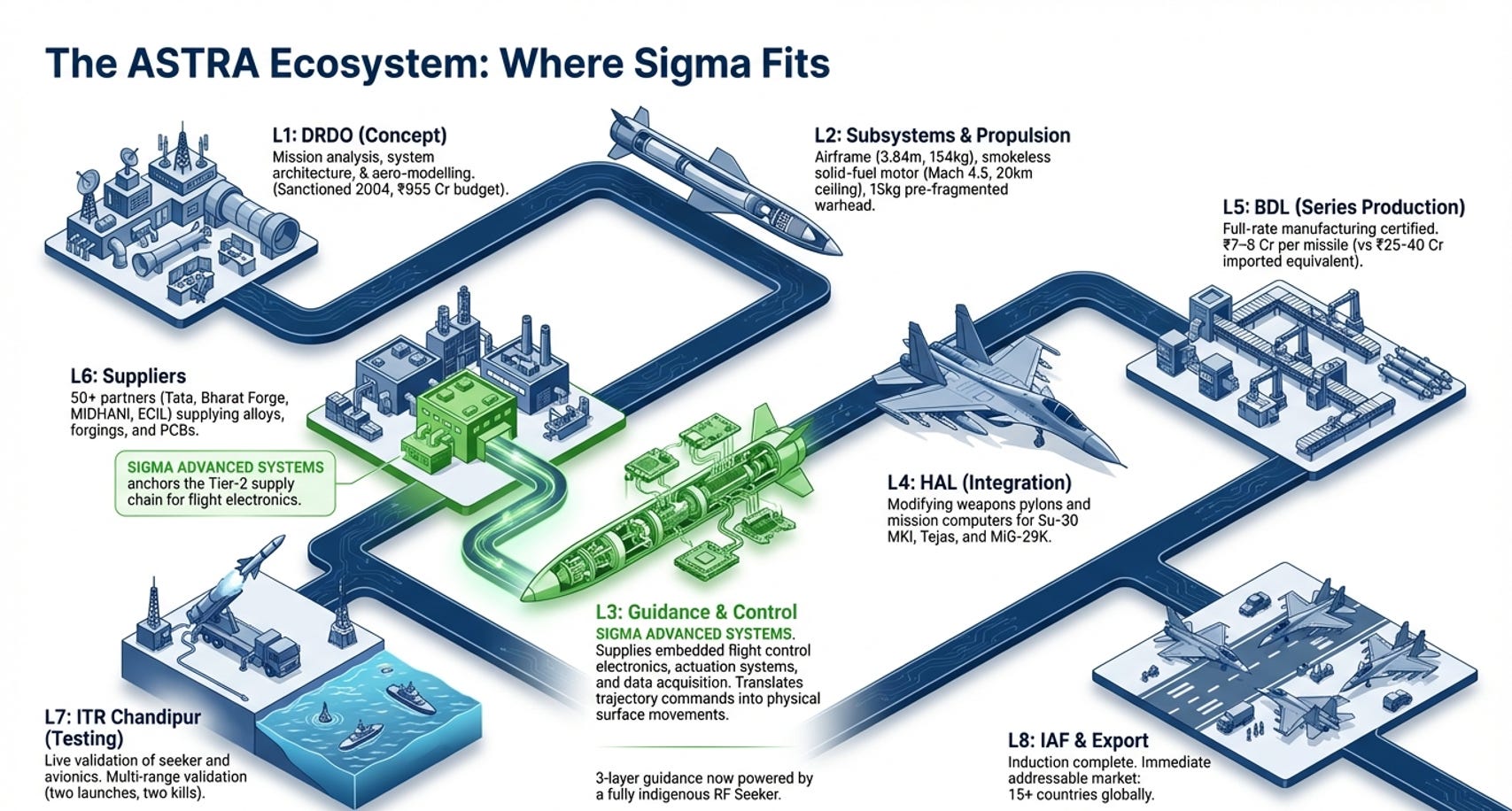

ASTRA Air-to-Air Missile. India’s indigenous beyond-visual-range missile, currently operational on the SU-30 MKI at 80 kms range. ASTRA MkII, targeting 150+ kms, is in development. Sigma supplies electronics. The same pattern applies to qualification on Mk-I, which accelerates the path to Mk-II. The Indian Air Force wants more ASTRA. More ASTRA means more of what Sigma builds.

NGARM - is now officially designated Rudram-1 the Next Generation Anti-Radiation Missile. This is the most strategically significant and most misunderstood element of Sigma’s IP portfolio. An anti-radiation missile does something that sounds almost impossibly precise: it homes on the electromagnetic emissions of an enemy radar system and destroys it. The seeker in an ARM must detect, classify, and track radar frequency emissions while the missile is moving at supersonic velocity through contested airspace. The electronics required for this are among the most demanding in any weapons programme. The radio frequency sensing and electronic warfare engineering at their core the ability to identify and interrogate an electromagnetic signal, to classify it, to lock on it is essentially the same capability stack required to detect, classify, and neutralise a drone threat. Sigma built this capability for DRDO. Sigma is now commercialising it, under a different name, through its partnership with Indrajaal. The market has not connected these dots.

Sunil Kumar, Dhamodhar Reddy, Rekha Valluri, Sanjay Pukalay, Sai Mallela, and Vamsi Vellanki, Varu Valluri & Kiran Raju")

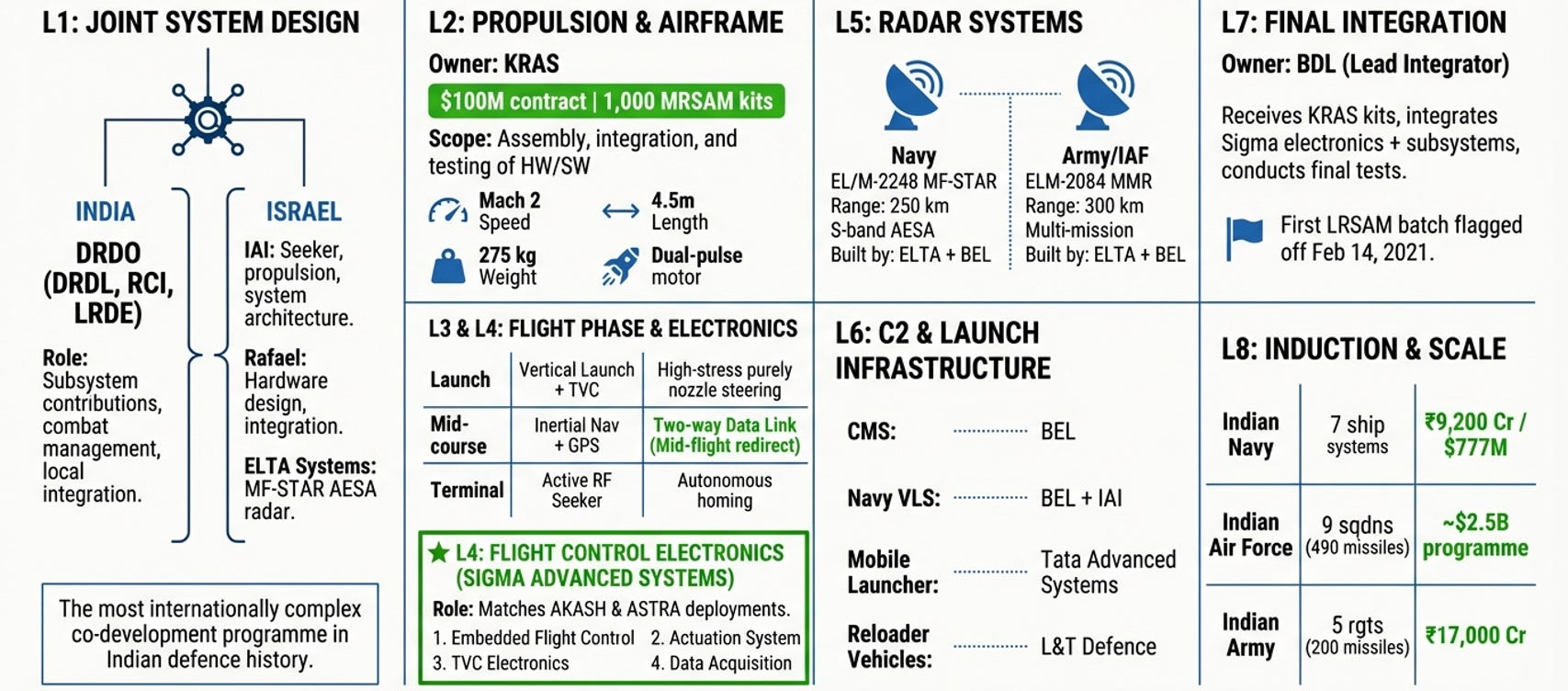

LRSAM and MRSAM the Barak-8 Family. The India-Israel joint programme is the crown jewel of the Indian Navy’s air defense doctrine. A $2.5 billion contract for the land-based Medium Range SAM for the Indian Army. LRSAM for the Navy. The consortium includes IAI, Rafael, BEL, L&T, BDL and Sigma. Being on the Barak-8 supply chain alongside IAI and L&T is the defence electronics equivalent of being a named Tier-1 supplier on the iPhone. The programme has decades of active service and ongoing production cycles ahead of it.

SU-30 MKI Avionics. 272 SU-30 MKI fighters form the backbone of India’s air superiority. Sigma supplies flight data recorders and antenna control systems for this fleet. Every time an IAF pilot scrambles from Jodhpur or Pune, there is a meaningful probability that Sigma’s electronics are managing the aircraft’s communication and recording its flight data.

Submarine and Naval Electronics. Torpedo rudder control electronics. Power distribution systems for naval platforms. LiDAR-based sensing for submarine applications. The companies qualified for submarine programme electronics supply are extraordinarily few. Sigma is one of them. The Indian Navy is in the middle of the largest submarine modernisation programme since independence — P-75I, six new submarines. The electronics requirements are substantial.

Economies of Learnings — Why Defence Qualification Compounds

In commercial technology, today’s product is next year’s legacy. Products depreciate. In defense systems, qualifications appreciate. Once you are qualified to supply AKASH, your path to AKASH NG is dramatically faster than any new entrant’s. Once you are on the Barak-8 supply chain, the relationships, the security clearances, the production process documentation, all of it is in place for the successor programme. Sigma has been compounding these qualifications since 1994.

The client list visible on Sigma’s own website HAL, BDL, BEL, DRDO, L&T, Tata Group, Cochin Shipyard, ISRO, Rockwell Collins, Motorola. It is a list of decades-long institutional relationships.

SECTION 02

The Shell and the Soul

How a dead telecom company became a listed defence platform and what the financial footprints reveal

Megasoft Limited was incorporated in 1999. For its first decade it made legitimate telecom software billing systems, mediation platforms, number portability solutions for carriers around the world. Then the market consolidated around companies like Amdocs and CSG Systems with hundred-country presences, and Megasoft found itself a mid-tier player in a game that was rapidly becoming winner-take-most. Revenue peaked somewhere above ₹100 crore in the early 2010s and began a slow, then accelerating, then terminal descent.

By FY2024, Megasoft had essentially zero operating revenue. It was alive in a technical sense it had a BSE listing, an NSE listing, a company secretary, and a board that met quarterly to report on the absence of meaningful business. It was not alive in any economic sense. What it had was regulatory capital: a valid listed entity with active exchange memberships. In India, that is worth something.

Here is the mechanism, stripped of its legal complexity. Sigma Advanced Systems Private Limited was a real business with real assets. Megasoft was a listed shell with real regulatory clearances. An NCLT-approved scheme of arrangement merged the private entity into the listed one, issuing new shares to the private company’s shareholders in exchange for the private company’s assets being absorbed into the listed entity. The combined entity was then renamed. The private company became the public company. The soul moved into the shell.

But here is what the transaction created that most have not processed: on December 31, 2025, Sigma Advanced Systems Limited issued 10.25 crore new shares to Chintalapati Holdings Private Limited. This gave Chintalapati 46.31% of the combined entity. The prior promoter group Ramanagaram Enterprises, which itself had absorbed Sri Power Generation’s earlier stake retained approximately 24.91%. Total promoter holding: 71.22%. Public float: 28.78%.

WATCH: The Annual Report Is the Most Important Document You’ll Read This Year

SECTION 03

The Brilliant Wreck

What ₹213 crore bought, and what Rcapital didn’t finish before leaving

The Nasmyth Group is named, in the way that British engineering companies often are, after a founder whose actual role in the company’s modern incarnation is purely titular. James Nasmyth invented the steam hammer in 1839 and helped make the Industrial Revolution physically possible. The companies that eventually became the Nasmyth Group have been making precision aerospace components in the UK Midlands for almost 75 years. They are not startups. They are, in the best British engineering tradition, institutions that have outlasted the industries that originally created them and found new ones to serve.

Sigma paid GBP 17.8 million approximately ₹213 crore for 100% of a company generating GBP 60 million in annual revenue. That is a 0.3x revenue multiple. Comparable UK precision engineering businesses transact at 0.8-1.2x revenue in private markets. The discount is a message.

Clayton Christensen’s Innovator’s Dilemma describes how new entrants can disrupt established players by initially operating at the low-margin, lower-quality end of a market, building capabilities, and then moving up the value chain. Sigma is, in a sense, applying the Innovator’s Dilemma to the global aerospace supply chain.

India’s position in global aerospace low-cost, improving quality, rapidly developing capabilities mirrors the position that Taiwan and South Korea occupied in semiconductors in the 1980s, or that Japan occupied in automotive in the 1960s. The disruptive trajectory is: start with lower-value components, prove quality, move up to higher-complexity parts, earn programme qualifications, eventually become indispensable.

The Nasmyth acquisition is a shortcut on this trajectory it acquires the programme qualifications rather than building them. But the shortcut introduces complexity that organic capability building does not: integration risk, culture management, currency exposure, and the challenge of maintaining quality standards during ownership transition.

The message: Nasmyth nearly died. Pre-COVID, the company was generating over GBP 80 million in revenue across ten sites in the UK, the US, the Philippines, and India, supplying Rolls Royce and Boeing with the precision-machined components and special-process treatments that jet engines and airframes require. Then commercial aviation demand collapsed. Revenue fell sharply. The cash position deteriorated. The existing debt structure became unsustainable. In February 2022, a UK private equity firm called Rcapital Partners stepped in with a £20 million debt refinancing and rescued the business.

Three and a half years later, Rcapital exited. Their own description of the experience: ‘one of the most challenging turnarounds we have faced, with the business undergoing a major operational and financial restructuring.’ By the time they sold, revenue had recovered to GBP 60 million and the business was their exact words ‘profitable at an EBITDA level.’

Stop there. ‘Profitable at an EBITDA level’ is the most carefully chosen phrase a distressed asset specialist can deploy. It means profitable before interest, before depreciation, before any return on the debt that financed the rescue. For a precision engineering company with factories full of CNC machines and heat treatment furnaces and chemical processing equipment, depreciation is not an accounting abstraction. It is a real, ongoing consumption of capital that must eventually be replaced. A business generating 8% EBITDA margin on GBP 60 million GBP 4.8 million might see a significant portion of that absorbed by depreciation, interest on the Rcapital debt, and working capital consumption from a growing order book. The gap between ‘EBITDA profitable’ and ‘generating free cash flow’ can be large and uncomfortable.

The critical analytical question is not ‘what did Sigma pay?’ It is ‘why was Rcapital a specialist in distressed assets who bought cheap and spent three years improving the business willing to sell for what appears to be below fair value?’

There are two non-exclusive answers. First: Rcapital operates closed-end funds. They have investment timelines. They must return capital to their investors regardless of whether the underlying business has fully completed its recovery. The fund lifecycle, not the business lifecycle, drives the exit timing. Second: the business may have more turnaround work remaining than the headline numbers suggest. Both can be true simultaneously.

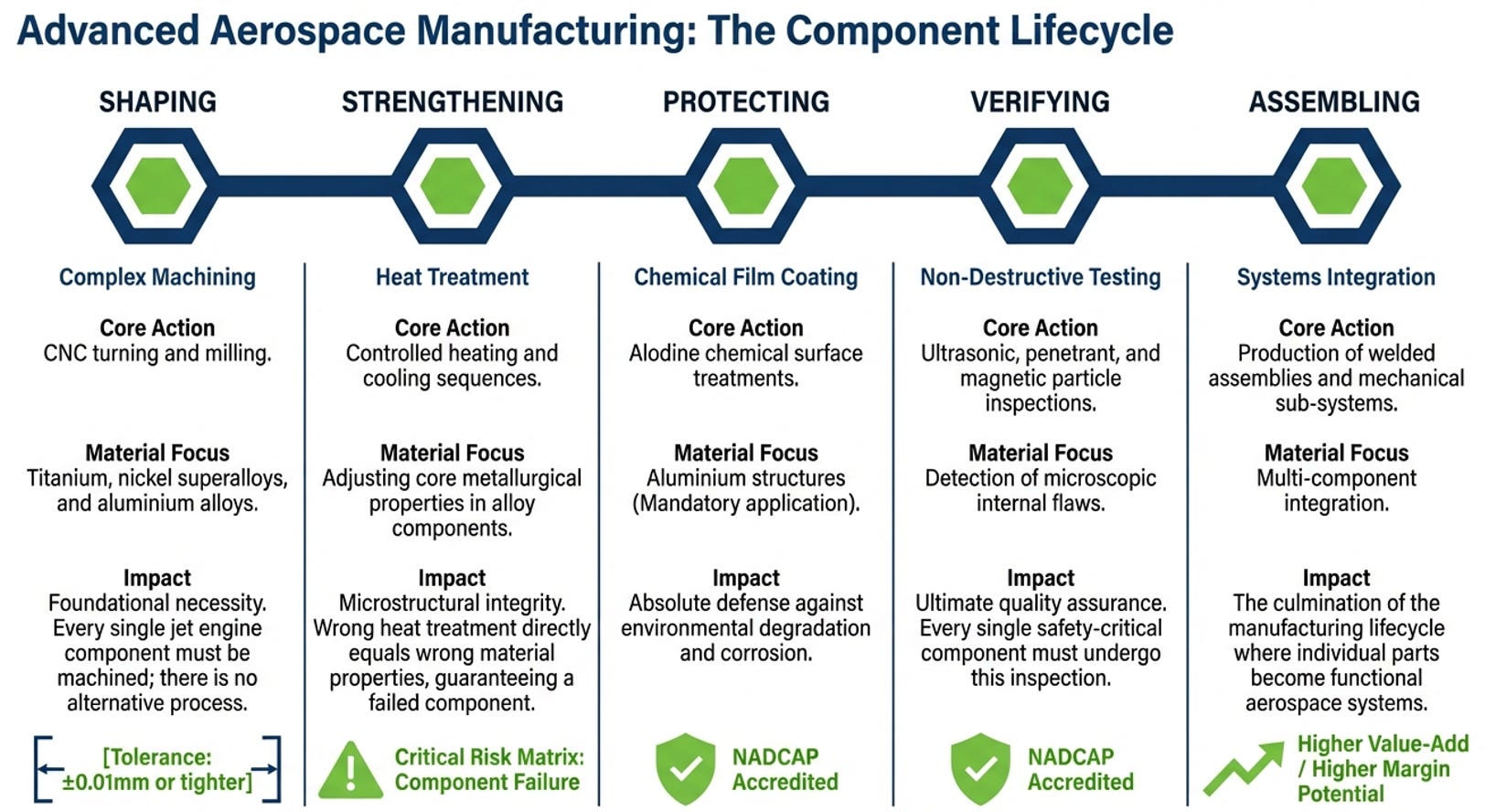

The NADCAP Moat; Why This Is Not Just a Factory

The most underappreciated asset in the Nasmyth acquisition is not the revenue, the customers, or the workforce. It is the NADCAP (National Aerospace and Defense Contractors Accreditation Program) accreditation portfolio. NADCAP the National Aerospace and Defense Contractors Accreditation Program is the aerospace industry’s highest-level quality certification for special manufacturing processes. Getting it requires formal audits by industry-experienced assessors, a findings resolution process, committee approval, and ongoing re-audits every six to eighteen months. Initial certification for a single process category takes twelve to eighteen months of intensive preparation.

What this means competitively: no one can simply decide to compete with Nasmyth for Rolls Royce business. They must first earn NADCAP accreditation (eighteen months minimum per process category), then complete Rolls Royce’s own supplier qualification (another twelve to twenty-four months, including test lots, first article inspection, and production part approval), before a single production component ships. The total journey from ambition to first revenue is three to five years. Nasmyth has already made that journey. The certifications exist. The relationships exist.

Two embedded options, one must look at

The Boeing Recovery Option. Boeing has been in an operational crisis. The 737 MAX door-plug incident in January 2024 triggered an FAA production cap at 38 aircraft per month, versus a planned 52. Boeing’s own recovery plan targets a return to higher production rates through 2026-2027. If Nasmyth’s revenue is correlated to Boeing’s production rates which, for a Tier-1 Boeing supplier, it is then Nasmyth’s current GBP 60 million baseline is artificially depressed. As Boeing normalises, Nasmyth’s revenue may grows automatically. Sigma paid for a GBP 60 million business.

The India Arbitrage Option. A UK precision machinist with aerospace experience earns approximately GBP 40,000 per year. An equivalently capable Indian machinist at a defense-qualified facility earns approximately ₹10 lakh around GBP 9,000. A 4.5x labour cost differential for broadly equivalent skills. Once Sigma earns NADCAP accreditation for its Hyderabad facility, a two-to-three-year investment, it can manufacture components for Rolls-Royce programmes from India at dramatically lower cost, ship them to Nasmyth’s UK facilities for final quality certification and delivery, and retain the margin difference. The OEM does not care where the part was machined. (Manthan - are we sure here?) It cares only that the part meets specification and carries the right certification. This arbitrage requires no new customers. It applies immediately to Nasmyth’s existing programme portfolio. Even a five-percentage point margin improvement on GBP 60 million revenue is GBP 3 million of additional annual EBITDA substantially more than Sigma’s entire annual interest expense.

OPTIONALITY The ₹450 Crore Investment Plan Blueprint for the Arbitrage

Sigma has announced plans to invest ₹450 crore approximately GBP 42 million in expanding capabilities and building capacity. This number alarms bears because it is unfunded in any public communication. It should also fascinate bulls, because it is the exact investment required to build the Indian manufacturing base that makes the labour cost arbitrage real. NADCAP certification for an Indian facility, investment in aerospace-qualified CNC equipment, building the process control documentation infrastructure these are the line items behind the ₹450 crore figure. The concern is genuine: no specific source of funds, no timeline, no milestone structure has been disclosed. This is the most important governance gap currently outstanding. But the ambition behind the number, properly understood, is strategically coherent.

SECTION 04

Twenty Crore for a European Network

In February 2026, Sigma paid ₹20 crore for 51% of AS Strategic Private Limited, a Delhi-based defense company. The announcement was made in the same month as the rebranding and the Indrajaal partnership and the ₹100 crore domestic MoD orders.

AS Strategic brings three specific things to the Sigma platform.

First: a ₹315 crore order book for calendar year 2026, described as primarily tied to ongoing European defense programmes.

Second: established joint ventures with Escribano, Arquimea, and AbraWorks three Spanish defense companies with active European Defense Fund participation.

Third: partnerships with four companies in the Czech-based CSG Group, including Excalibur International and Fábrica de Municiones de Granada, alongside Yugoimport SDPR, Milkor, and Truvelo Armory.

The Escribano relationship deserves specific attention. The European Defense Fund EUR 8 billion for 2021-2027 finances collaborative defense R&D across EU member states. The European defense procurement cycle has been dramatically accelerated by the Russia-Ukraine war: Germany has committed EUR 100 billion to defense modernisation, Nordic and Baltic nations are rebuilding capabilities, and the entire NATO alliance is in the fastest rearmament cycle since the Cold War. Escribano is positioned in this cycle. AS Strategic’s relationship with Escribano is Sigma’s pathway into it.

But here is the insight that does not appear in any press release about this acquisition: AS Strategic currently outsources its manufacturing. It wins contracts and farms production to third parties, capturing the programme management and integration margin while losing the manufacturing margin. Sigma plans to bring that manufacturing in-house to its Hyderabad facility, and for European programmes requiring Western provenance, through Nasmyth in the UK. The manufacturing margin that currently flows out of the AS Strategic P&L is retained in the Sigma group. At ₹315 crore of contracts, even an eight percent manufacturing margin improvement represents ₹25 crore of incremental annual EBITDA more than the acquisition cost. This is not a speculative synergy. It is simple arithmetic applied to a disclosed business model change. This shows you the management’s thinking behind the decision.

SECTION 05

The Counter-Drone Gold Rush

Why the most important partnership in this story happened by design, not accident

There is a tempting narrative about the Sigma-Indrajaal partnership: agile Indian defence company pivots to the hottest emerging military technology segment, announces partnership with impressive-looking AI company, stock re-rates on counter-drone enthusiasm. The actual story is more interesting.

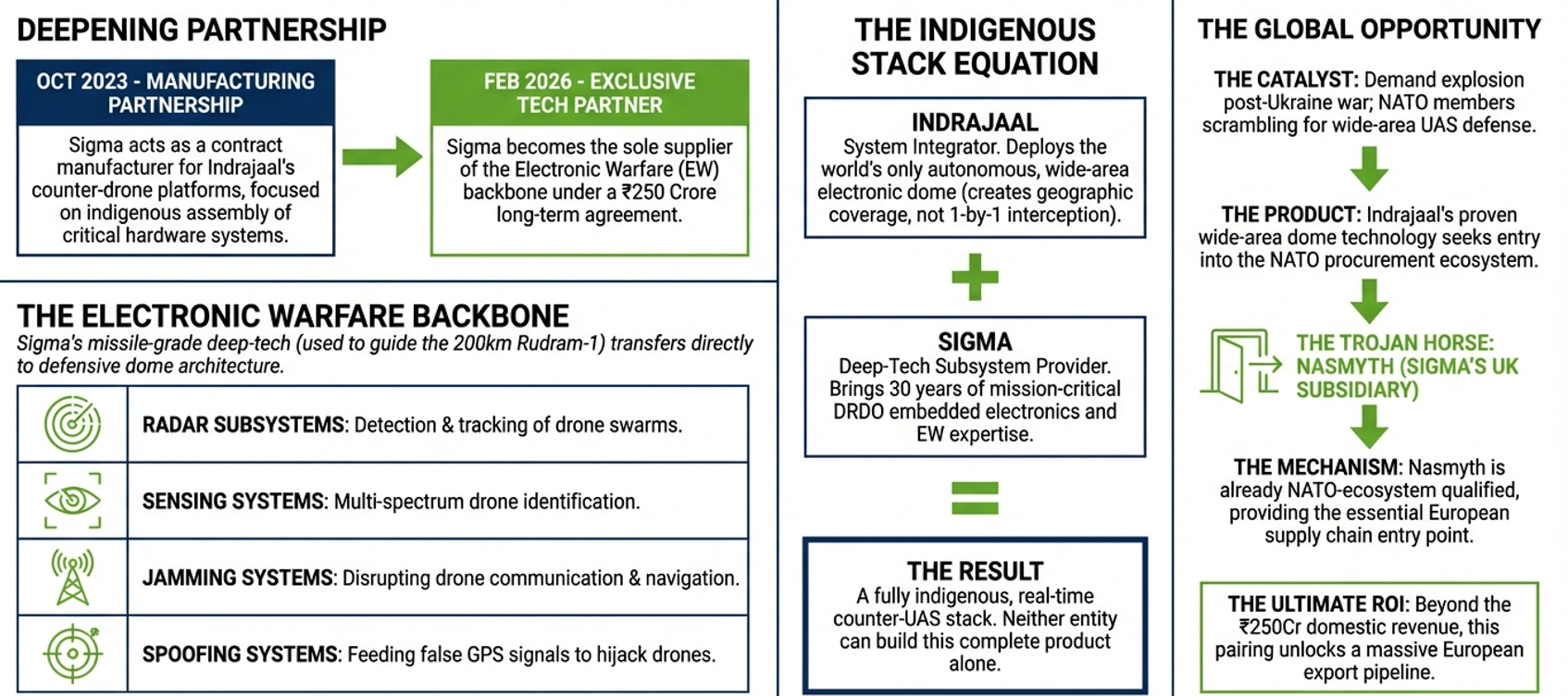

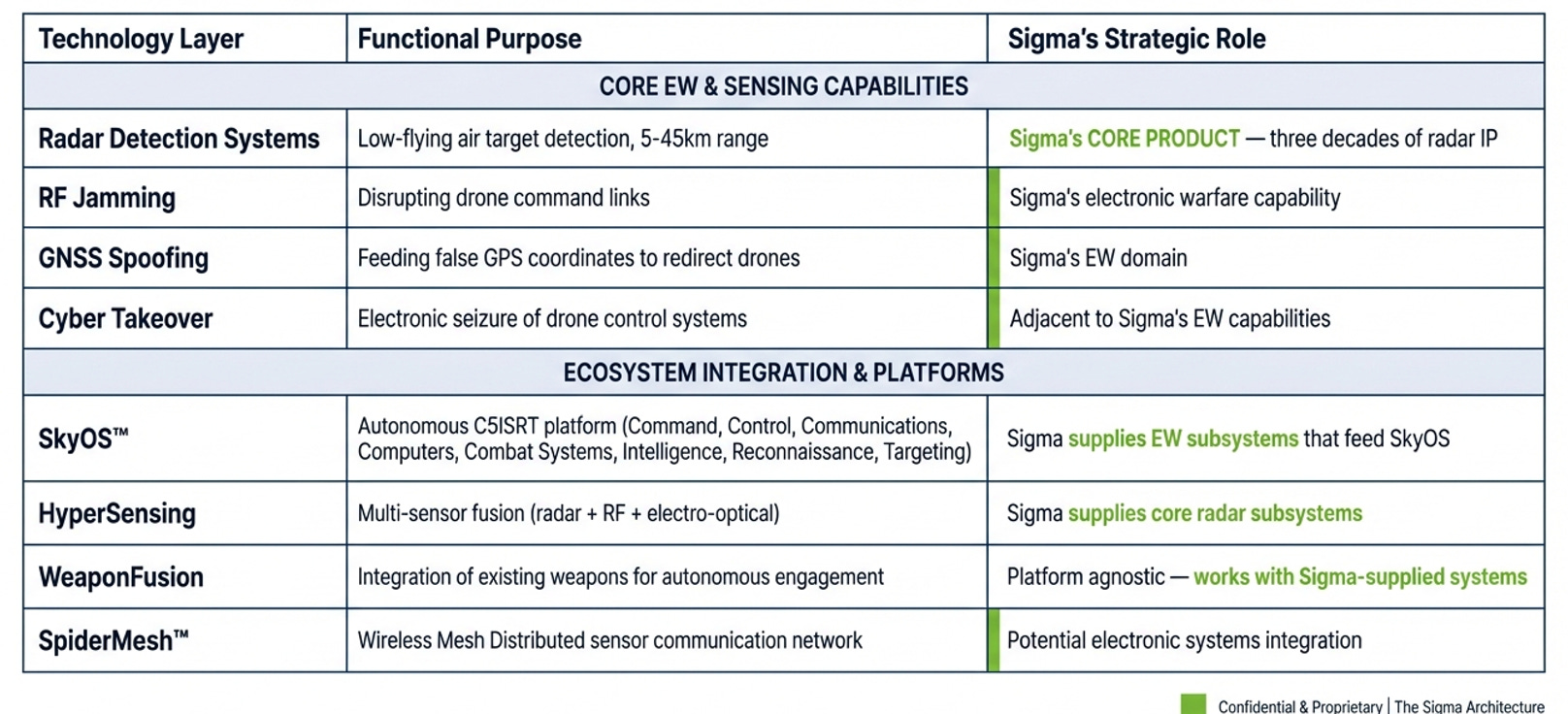

Indrajaal Drone Defense, developed by Grene Robotics, is the world’s only and that word is significant, because it is specific and verifiable fully autonomous wide-area counter-drone system. Most counter-drone solutions are point-defence: they protect a single asset from a specific attack vector. Indrajaal claims area coverage of up to 4,000 square kms through a twelve-layer technology stack that includes radar detection, RF jamming, GNSS spoofing, AI-guided interception, and an autonomous command platform called SkyOS. It has an 80-acre test facility in Hyderabad. Senior Indian Army generals have attended demonstrations and gone on record calling it ‘groundbreaking.’ In November 2025, it launched India’s first Anti-Drone Patrol Vehicle a mobile system that neutralises drone threats while in motion, something that no competing platform currently offers.

Sigma is not a passive partner in this ecosystem. It is the exclusive supplier of the radar, jamming, and spoofing subsystems the technological backbone of every Indrajaal platform. The year-one contract expectation is ₹250 crore.

Why This Partnership Is Not a Pivot

Here is the insight that reframes the entire Indrajaal relationship. Sigma develops tactical reconnaissance radars with operational ranges from 5-45kms, specifically engineered to detect low-flying targets cruise missiles, drones, small aircraft against ground clutter. This is one of the hardest problems in radar engineering. Ground clutter is the electromagnetic noise generated by the ground itself reflecting radar signals back at the receiver. A low-flying target inside this clutter is almost invisible to a conventional radar. Sigma spent three decades solving this problem for DRDO, building radars that could find and track these signatures for the NGARM programme and for border surveillance applications.

The drone threat is, in electromagnetic terms, structurally identical to the low-flying target problem Sigma has been solving since the mid-1990s. A weaponised commercial drone is a small, slow, low-flying radar target moving against ground clutter. Sigma’s radar technology developed for entirely different purposes is the exact solution. Sigma did not pivot to counter-drone. Counter-drone came to find Sigma’s pre-existing capability.

OPTIONALITY — The NATO/EU Expansion via Nasmyth the ₹1,000 Crore Question

Nasmyth’s UK presence creates a specific pathway that Indrajaal cannot access independently: direct engagement with European and NATO defense procurement ecosystems. European NATO members are in a counter-drone procurement emergency. Ukraine has changed the threat calculus permanently. Every European defense ministry now needs a credible answer to the drone swarm question. Indrajaal’s technology, supplied through a UK-headquartered precision engineering company with established OEM relationships and Western certification infrastructure, has a plausible path to European procurement that a direct India-to-NATO pitch does not. If Indrajaal achieves even a two percent share of the European C-UAS market over the next five years a market estimated at USD 4+ billion Sigma’s exclusive radar and EW supply position generates annual revenues an order of magnitude above the current ₹250 crore estimate.

SECTION 06

The Optionality Map

Five doors that are now open and what is through each one

The standard way to value a company is to project its current business forward and discount those cash flows back to a present value. This method is correct for stable, predictable businesses. It is systematically wrong for companies undergoing genuine strategic transformation, because it assigns zero value to all the options that transformation creates. Sigma, right now, has more real options than almost any comparable company in the Indian defence sector.

Option 1: The New Programme Pipeline. India’s defence indigenisation is accelerating at its fastest pace since independence. AKASH NG. ASTRA MkII. QRSAM. P-75I submarine electronics. The Indian Navy’s next-generation destroyer suite. Each of these programmes will require electronics that meet the same standards as the programmes Sigma already supplies. In defence procurement, incumbency is the strongest competitive advantage: the company that built ASTRA Mk1 is the first call when ASTRA MkII needs an electronics supplier. Sigma is that company for multiple programmes simultaneously.

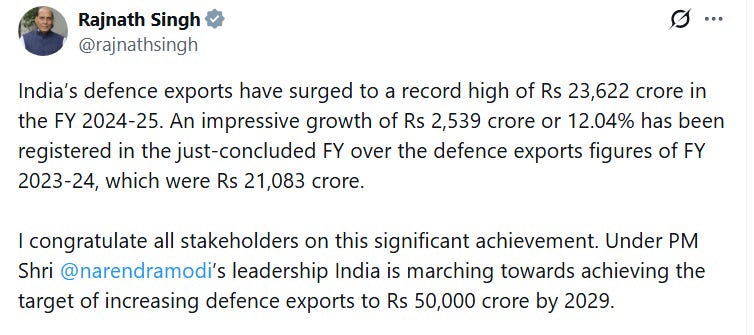

Option 2: The Defense Export Machine. India has set a defense export target of ₹50,000 crore by 2028-29. Indian defense exports have grown from ₹1,941 crore in FY2017 to over ₹23,622 crore in FY2025 an eleven-fold increase in 8 years. The export categories that are growing fastest electronics, EW systems, missiles, surveillance are precisely where Sigma has deployed IP. A company with Rolls Royce relationships in the UK, European defense programme access in Spain and the Czech Republic, and thirty years of electronics qualification for Indian military platforms is positioned to ride this export wave in a way that almost no other Indian private defense company is.

Option 3: The PSU Capacity Gap. BEL has an order book of approximately ₹60,000 crore and is already running at capacity. ECIL is similarly constrained. DRDO’s own labs are overwhelmed with development work. The Indian armed forces’ procurement rate has permanently outstripped the public sector defence electronics ecosystem’s ability to supply it. Every programme that BEL cannot resource on the required timeline is a potential Sigma opportunity. The queue is long and growing.

Option 4: The Indrajaal Winner-Take-Most Scenario. Counter-drone systems have a specific competitive dynamic in the markets that matter most: once a wide-area C-UAS system is installed at a border corridor or critical infrastructure site, integrated with the existing command and communication infrastructure, and used to train local operators, switching costs become enormous. The system that gets embedded first tends to stay. If Indrajaal achieves embedded status in three or four major Indian deployments say, the Punjab border corridor, the Mumbai port complex, and one military cantonment the replacement cost for any competitor becomes prohibitive. Sigma’s exclusive supply position then becomes one of the most durable revenue streams in Indian private defence. The exclusivity clause is the key word. Sigma does not share this customer.

Option 5: The Global Aerospace Sourcing Shift. The ‘China+1’ supply chain diversification where global manufacturers build parallel capacity outside China has been the most discussed structural trend in manufacturing since COVID. In aerospace specifically, the shift is accelerating. Rolls Royce has publicly stated its intention to increase Indian sourcing. Airbus is expanding its Indian supply base. Boeing’s Tata joint venture in Hyderabad is already producing 737 aerostructures. Sigma, with Nasmyth’s OEM relationships on one end and its own DGQA-qualified Indian facility on the other, is the most natural routing mechanism for this shift. Western OEM requirement flows through Nasmyth’s existing qualification and relationship, gets produced at Indian cost in Hyderabad, and re-enters the Western supply chain through Nasmyth’s UK infrastructure. No new customers required. Just the geography of production changes. The margin improves on both ends.

SECTION 07

Seeds of Failure

What can unravel everything and the base rates that tell you how often it does

Every thesis has a mirror. This one is no different. The seeds of failure below are not invented risks manufactured for balance. They are specific, observable failure modes with historical precedent. An investor who ignores them is not bullish, they are uninformed.

RISK The Nasmyth Integration Risk Most Dangerous, Most Overlooked

The most catastrophic single failure mode: management distraction during integration creates disruption in Nasmyth’s production quality or delivery performance. Rolls Royce places Nasmyth on a Controlled Shipping Level 2 process. Boeing initiates a Supplier Quality Management escalation. In aerospace supply chains, recovering from a formal OEM performance intervention requires sustained improvement over twelve to eighteen months during which component volumes are typically reduced and future contract negotiations are affected. The NADCAP accreditation may be moved to a more frequent re-audit cycle. The customer relationships that are the core value of this asset can degrade faster than they can be rebuilt. Historical base rate: approximately 25% of cross-border acquisitions of UK precision engineering businesses by non-UK buyers experienced significant operational disruption in the first eighteen months. Of those, half recovered within two years. The other half saw permanent revenue base erosion. A management team running three simultaneous integrations across three geographies, in a company structure that is less than six months old as a listed entity, is a stretched management team.

RISK The ₹450 Crore Funding Gap The Number That Must Be Answered

The expansion capital commitment is unfunded in any public document. The options operating cash flow, new debt, equity issuance each carry specific costs for shareholders. An equity raise at current prices that exceeds ten percent of shares outstanding would be significantly dilutive.

RISK The Float Mechanism in Reverse What a 28.78% Float Means on a Bad Day

The same thin public float that produced 186% upside is capable of producing 50-60% downside on a single narrative-breaking data point. With minimal institutional ownership, there are no price-support buyers when retail sentiment reverses. A disappointing Nasmyth margin say, 7% rather than 12.5% combined with a delayed AS Strategic order book conversion, combined with an Indrajaal procurement stall, would create a narrative vacuum that a thin float cannot support. The three things do not need to happen simultaneously. One is sufficient to start the sequence.

Who owns the customer relationship owns the economics: In any supply chain, value capture is ultimately determined by who owns the customer relationship. An OEM (Rolls Royce) captures the highest margin because it owns the customer (the airline or air force). A Tier-1 supplier (Nasmyth) captures the next tier because it has direct OEM relationships. A Tier-2 or component supplier captures less because it sells to the Tier-1, not directly to the OEM. Sigma's strategy is explicitly about moving up this chain: from Tier-2 component electronics supplier (existing India business) to Tier-1 system integrator (AS Strategic's European programme access) to OEM-adjacent systems provider (Indrajaal, which integrates Sigma's subsystems into a complete platform that is then sold directly to government customers). Each step up the chain captures more value per revenue rupee. The question is whether Sigma has the management bandwidth to make this vertical ascent while simultaneously managing a UK manufacturing company.

The Ghost Becomes Visible

The ghost in the machine was always there. Thirty years of engineers in Hyderabad’s Hardware Park building the things inside India’s things the electronics that guided missiles, the avionics that recorded fighter flights, the processors that controlled submarine torpedoes. Invisible because serious defense technology companies are supposed to be invisible. Essential because the weapons they supply cannot afford to fail.

Now the ghost is listed on the NSE. And it has moved with a speed that either reflects genuine conviction from a management team that has been waiting a long time for this moment, or the urgency of a promoter who understands that the market’s attention is a depleting resource. The Nasmyth acquisition, the AS Strategic acquisition, the Indrajaal partnership, the MoD orders, the rebranding all of this happened inside fourteen months. Fourteen months is a very short time to integrate three businesses across two continents while simultaneously managing a newly listed entity’s regulatory obligations, investor relations, and governance infrastructure.

This is the tension at the heart of the investment. The foundation the thirty-year defense electronics heritage, the deployed technology on India’s most critical weapons platforms, the institutional relationships with DRDO, BDL, HAL, and the armed forces is extraordinary. The new construction on top of that foundation is four months old and moving faster than anything in Indian private defense has moved before.

The evidence for the quality of the foundation is overwhelming. The evidence for the quality of the new construction is still being gathered. In four quarters, we will know which one dominates the story.

Watch carefully. Read the annual report before any broker note. Follow the UK Companies House filing. Listen to what management says on earnings calls and more importantly, to what they don’t say. The rocks still have things under them.

The ghost in the machine is now listed. Whether it becomes a giant is still, at this moment, an open question.

Stay tuned, see you next time!

Until then… Share your views in the comments!

Disclaimer: This article is provided for informational purposes only and should not be considered as investment advice

P.S.: Abhay, Manthan/Writer- No Buy/Sell Recommendation!

If you enjoyed this Equity Autopsy, you’ll find many more like it in our AIC.

DISCLAIMER: This document is prepared for educational and informational purposes only. It does not constitute investment advice, a solicitation to buy or sell any security, or a recommendation of any kind. All data sourced from public filings (BSE/NSE/UK Companies House), company websites (sigmaadvsys.com, indrajaal.in), financial platforms (screener.in), and verified media reports as of April 2026. Market prices and financial figures are approximate and subject to change. Forward-looking scenarios may prove incorrect. Investing in securities involves substantial risk of loss. Past performance is not indicative of future results. The author holds no position in SIGMAADV as of the date of writing. Always conduct independent due diligence and consult a qualified financial advisor before making investment decisions.

This is an excellent breakdown of the company. The content reflects the amount of research done. I have been wondering how this company is flying below the radar of multiple Substack analysts (my term for the various stock related Substack posts). The answer is clear after reading the article. Doing a post on this company would require substantial amount of digging and you’ve done it. Kudos!

Any Corporate Governance issue ??🙏