How Northern Arc Is Rebalancing Its Way: Part 1

India does not have a capital shortage. It has a translation problem.

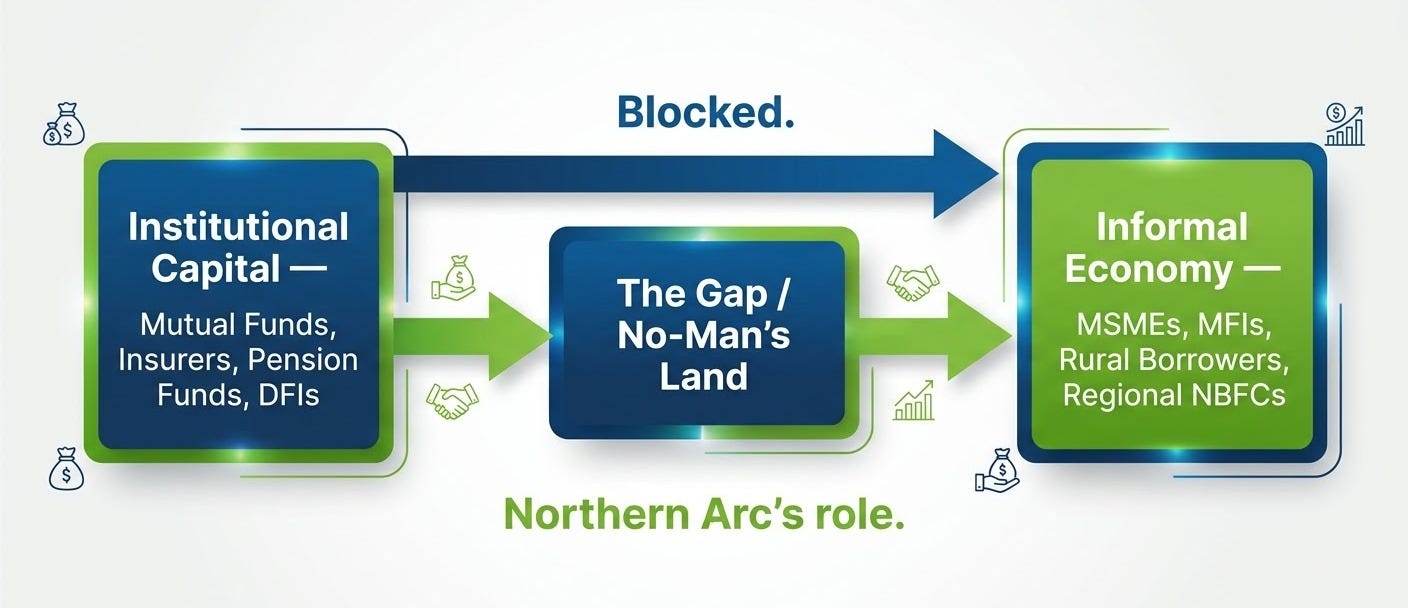

On one side of the ledger, you have ₹65 lakh crore in assets managed by mutual funds, insurance companies, and pension funds. These institutions are well-regulated, conservative, and sitting on yields they would prefer to improve. They are desperate for returns but have no mechanism to deploy capital into the parts of the Indian economy that actually need it.

On the other side, you have 63 million MSMEs, 500 million underbanked individuals, hundreds of regional NBFCs and MFIs a sprawling informal economy where credit is either unavailable or criminally expensive. These borrowers seem inherently riskier than their formal-sector counterparts, but they’re just opaque. They lack the documentation, ratings, and standardization that institutional investors require to deploy capital with confidence

The credit gap in India is not a shortage of money. It is a shortage of translation.

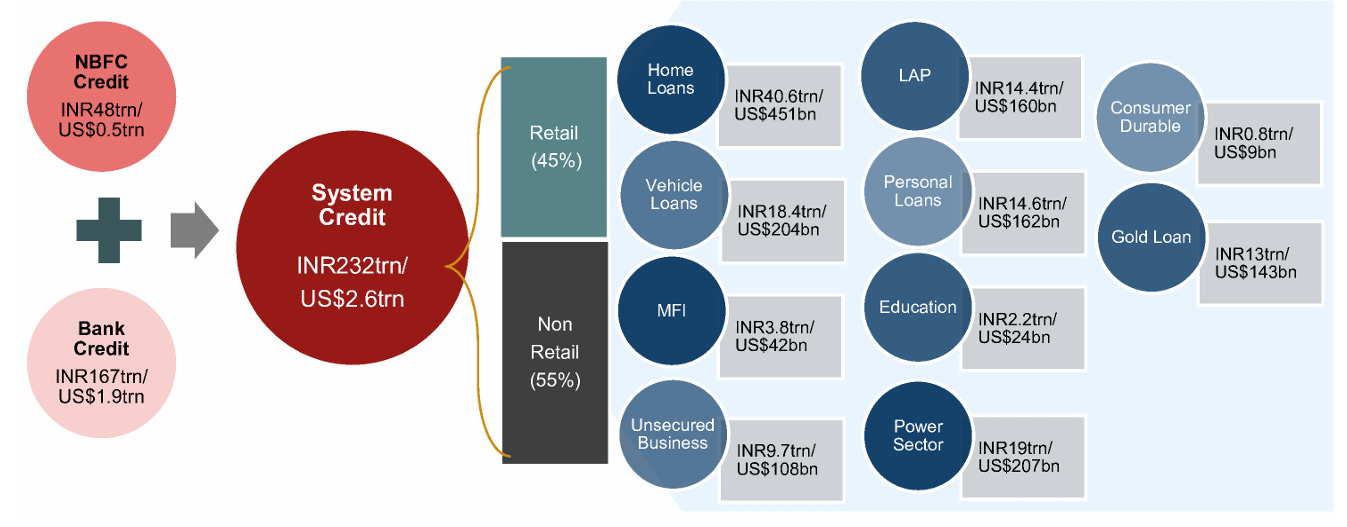

India’s financial system already carries over ₹230 lakhs crore of credit. Nearly half of this sits in standardized retail products like home, vehicle, and personal loans. Yet the segments that power the informal economy micro-enterprises and thin-file borrowers, still receive only a tiny fraction of institutional credit. The problem is not the absence of capital. It is the absence of mechanisms that can translate institutional capital into messy, small-ticket lending.

The ₹25–30 trillion credit gap that researchers and regulators cite is a measurement of this translation problem. The capital exists. The need exists. What doesn’t exist is a reliable, scaled mechanism to connect the two.

Banks theoretically fill this gap. In practice, they cannot. Banks run on standardization: audited statements, strong bureau scores, collateral, standard products. When a borrower doesn’t fit the template, the default answer is “no”.

Large institutional investors have the same problem in reverse. A pension fund cannot practically analyze and buy 200 separate bonds from tiny MFIs or MSME lenders. They need big, rated, standardized instruments they can slot into their risk frameworks.

Now here is where it gets interesting. For decades, India has tried to fix this with schemes: priority sector lending norms, MUDRA, SIDBI lines, NABARD programs. Most of these either pushed risk to the government balance sheet or produced compliance on paper without actually changing how capital flows.

That is what Northern Arc Capital is. Solve this translation problem.

The Credit Refinery

Think about what an oil refinery does.

Think about what an oil refinery does. Crude oil, as it comes out of the ground, is mostly useless. It is thick, dirty, and can’t be put straight into a car or aircraft. But hidden inside that crude are diesel, petrol, jet fuel, and LPG. The refinery does not create new oil; it transforms existing oil into standardized, usable products.

Northern Arc plays a similar role in credit. It does not “create” capital. It refines the form of credit risk that already exists in India’s informal economy.

Northern Arc is India’s crude credit refinery. It does not create capital. It transforms the form of capital that already exists into forms that markets can consume.

The crude oil in this system is the messy, illiquid loan books of small MFIs, local MSME lenders, and consumer financiers spread across semi‑urban and rural India. The borrowers, cash flows, and businesses are real. But from an institutional investor’s point of view, this risk is unrefined: undocumented, unstandardized, unrated.

Northern Arc’s job is to transform this crude risk into products that banks, mutual funds, insurers, and DFIs can understand and buy. It does this through:

Deep underwriting of originators.

Legal and structural design of transactions.

Credit enhancement, often through its own first‑loss capital.

Getting the deals rated.

Ongoing monitoring and audits

BUT, unlike a pure refinery, Northern Arc does not just process risk for a fee. It also holds risk on its own balance sheet. It lends directly to borrowers and takes first‑loss positions in many structures.

The Andhra Pradesh Lesson

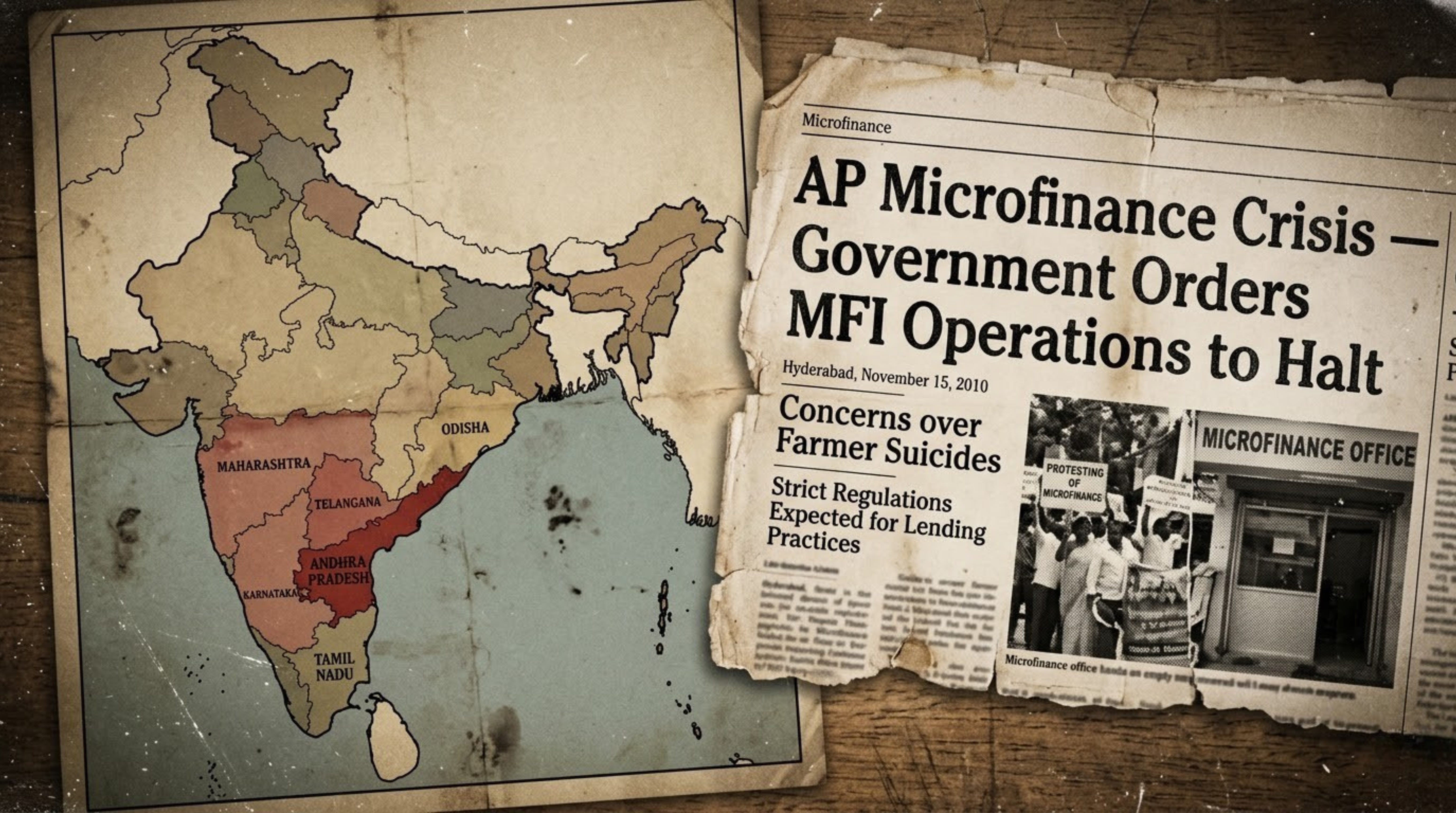

In 2010, the microfinance sector experienced what might be called its first proper near-death experience. The Andhra Pradesh government issued an ordinance that effectively halted MFI lending operations in the state. Overnight, the cash flow assumptions underlying billions of rupees of MFI debt became worthless. Banks and wholesale lenders who had deployed capital into the sector without understanding the underlying risk were suddenly holding assets nobody could price.

IFMR Capital the entity that would become Northern Arc was in the middle of this. But unlike its peers, it survived. The reason was structural: IFMR had designed its securitization transactions to require the originator to retain first-loss credit risk. This meant that when loan pool performance deteriorated, the originator absorbed the first wave of losses before institutional investors felt any pain. The alignment of incentives was baked into the transaction architecture.

Surviving the AP crisis while others didn’t wasn’t luck. It was proof of concept. The lesson that got hardwired into Northern Arc’s DNA was this: in a market where information asymmetry is severe and enforcement is weak, you cannot rely on ratings, representations, or warranties alone. You need the person who knows the risk best to have more to lose than anyone else when things go wrong.

Skin in the game is not Northern Arc’s marketing. It is the founding insight around which the entire business is constructed.

The Four Engines of the Machine

To understand Northern Arc now, think of a large airport. The infrastructure is the key.

An airport:

Provides infrastructure: runways, terminals, ATC.

Charges fees for take‑offs, landings, and services.

Sometimes also runs its own lounges, ground handling.

Northern Arc operates four distinct engines. Understanding how they interact is the key to understanding both the business model’s elegance and its tensions.

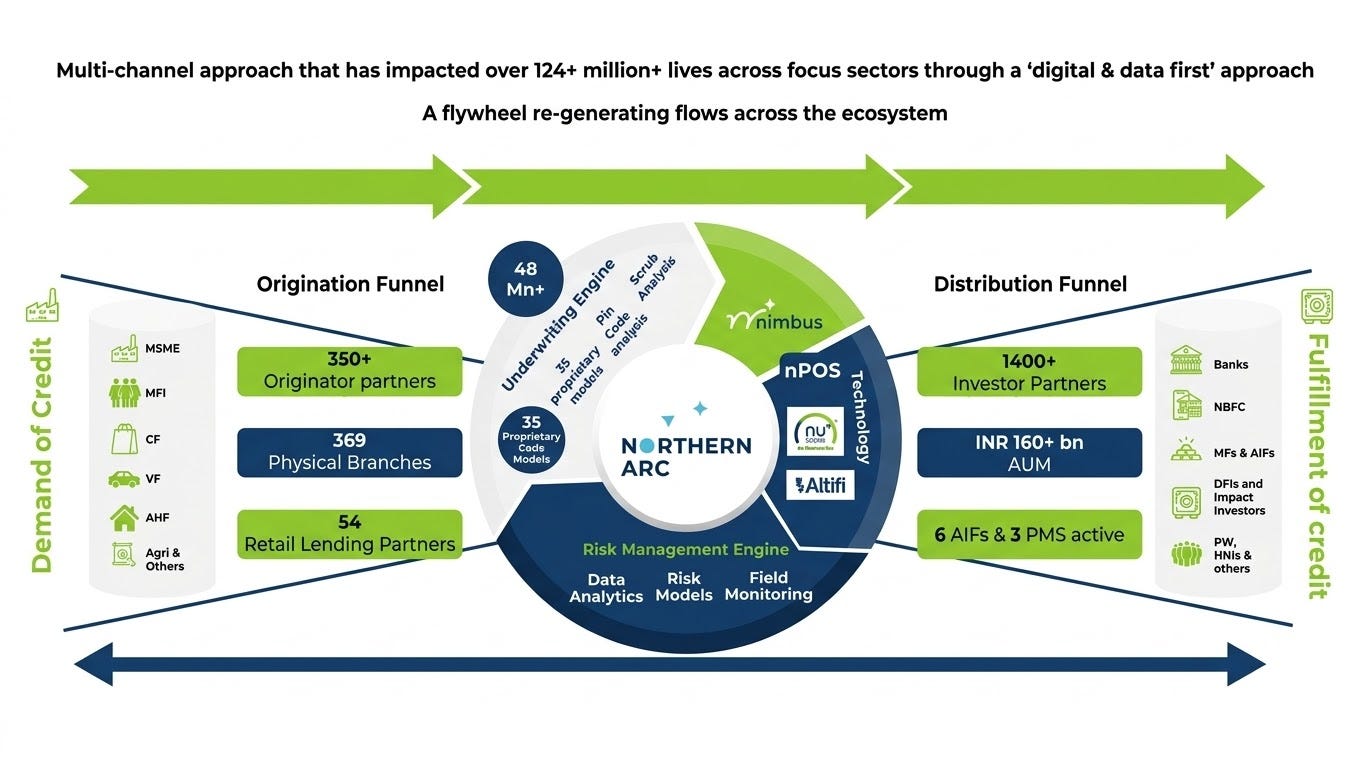

As the operator, Northern Arc manages the runways and the control tower. Through their proprietary tech stack (Nimbus, nPOS, NuScore), they process over 40 million data points, 30+ risk models, and execute constant field audits to monitor exactly which airlines are flying safely and which routes are turbulent. The result is a powerful trust bridge. Banks that would normally hesitate to lend to smaller fintech lenders begin extending capital because they rely on Northern Arc’s monitoring and audits as a proxy for their own due diligence.

They charge airport fees as placement fees, platform fees, and fund management fees for safely directing this traffic.

But crucially, Northern Arc also operates its own airline on select routes. When their control tower data shows a specific route is highly profitable and safe, they deploy their Direct-to-Consumer (D2C) lending arm to capture the full yield.

So, Northern Arc is basically two businesses wrapped into one:

A retail lender to hard-to-serve customers, and

A credit “market-maker” that connects dozens of niche lenders to capital and takes fees for it.

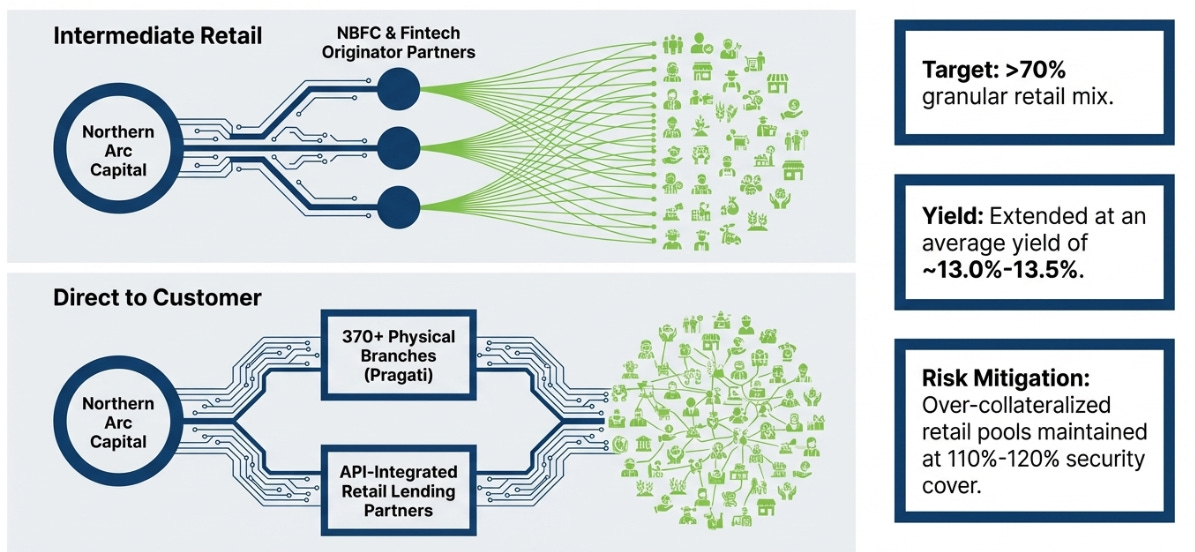

Engine 1 — D2C Lending: The Airline Northern Arc Chose to Operate Itself

If the platform is the airport, D2C lending is the airline Northern Arc decided to run on its own runways.

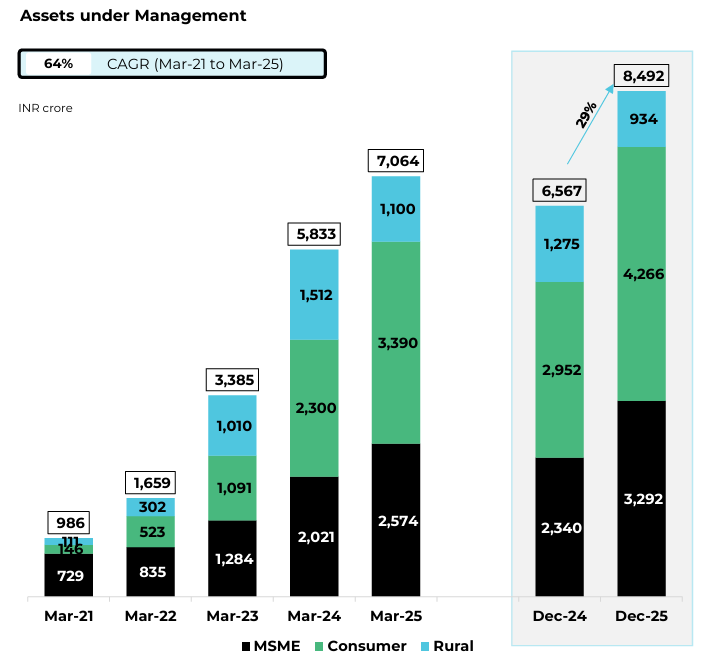

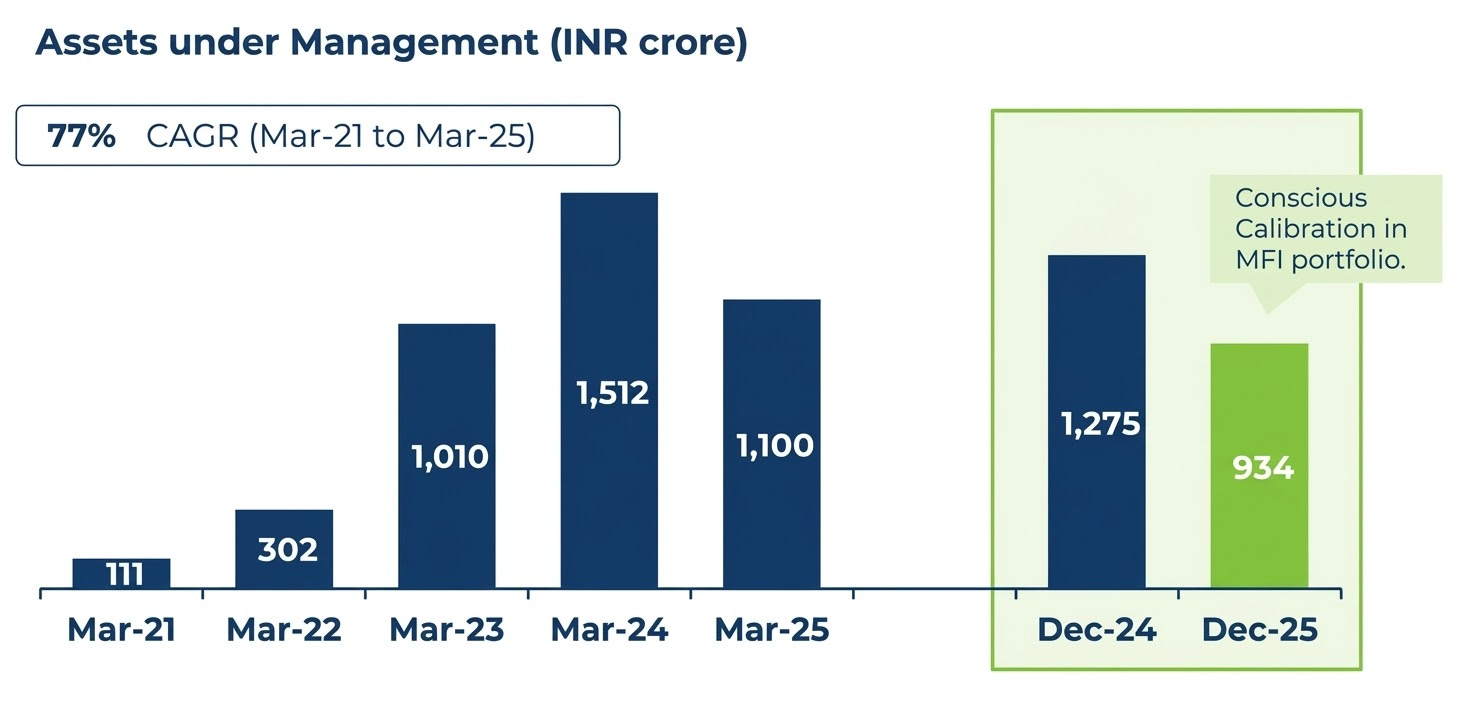

As of Q3 FY26, D2C constitutes ₹8,492 crore of its ₹15,121 crore total AUM, making it the largest single component at 56%.

From FY21 to FY25, D2C AUM went from ₹986 crore to ₹7,064 crore (63.6% CAGR) and D2C mix from 18.9% to 51.8%.

They are methodically swapping “wholesale, thin-spread” rupees for “retail, fat-spread” rupees, while accepting structurally higher credit cost.

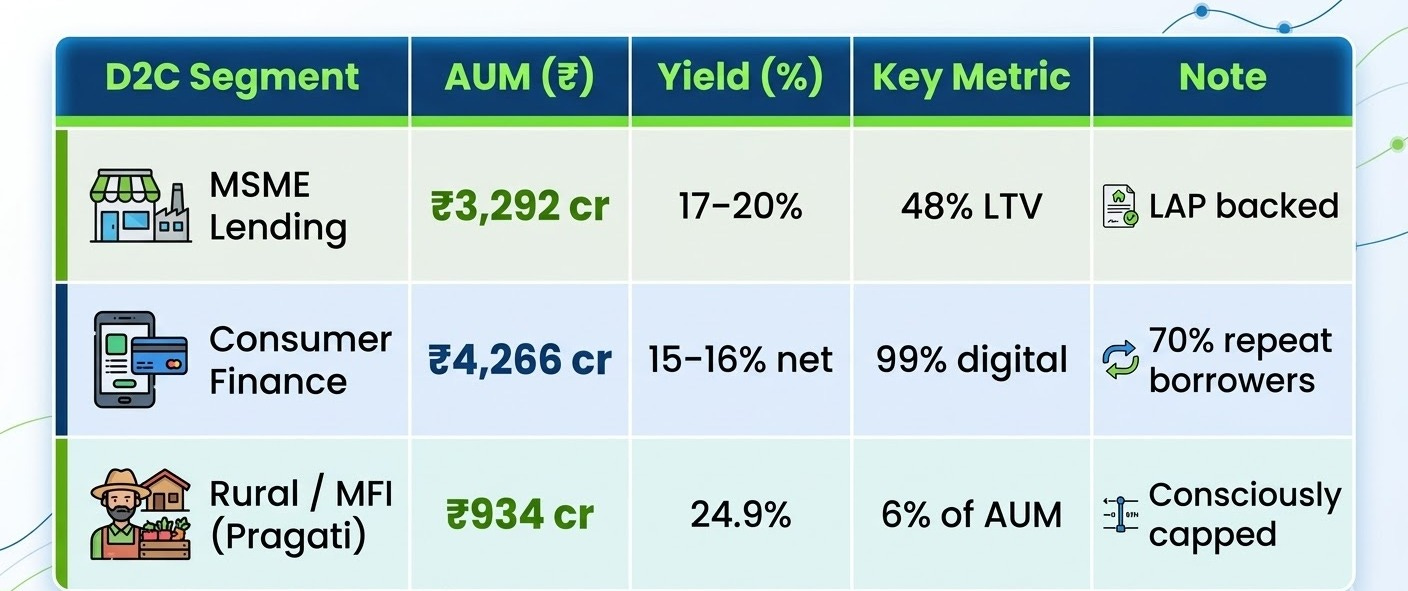

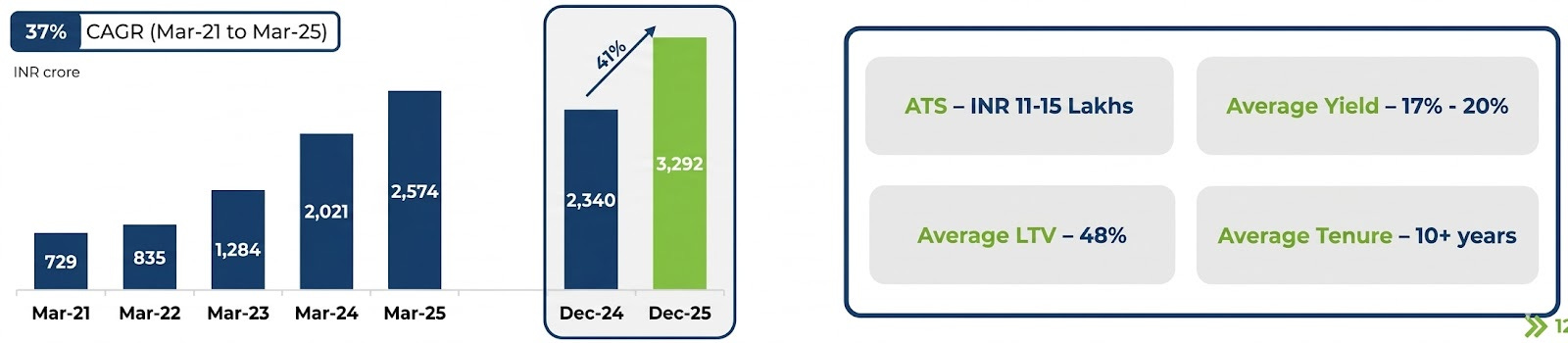

a.) D2C MSME Lending: LAP, working capital, and SCF

Northern Arc’s MSME book is built around Loan Against Property: tickets of ₹11–15 lakhs, loan-to-value (LTV) ratios of 48%, tenure of 3 - 10 years. These are semi-formal business owners, proprietorships, small manufacturers, traders who own property but lack the income documentation that a traditional bank requires.

The 48% LTV is important. It means Northern Arc has a cushion before a property sale doesn’t cover the outstanding loan.

A retail brand reaches customers in two ways: through its own large, fully controlled “flagship stores” where customers get the full brand experience, and through nimble “pop-up kiosks” placed inside other popular malls to catch foot traffic.

How Northern Arc’s MSME D2C fits in: Northern Arc uses a hybrid “phygital” (physical + digital) approach to source small businesses.

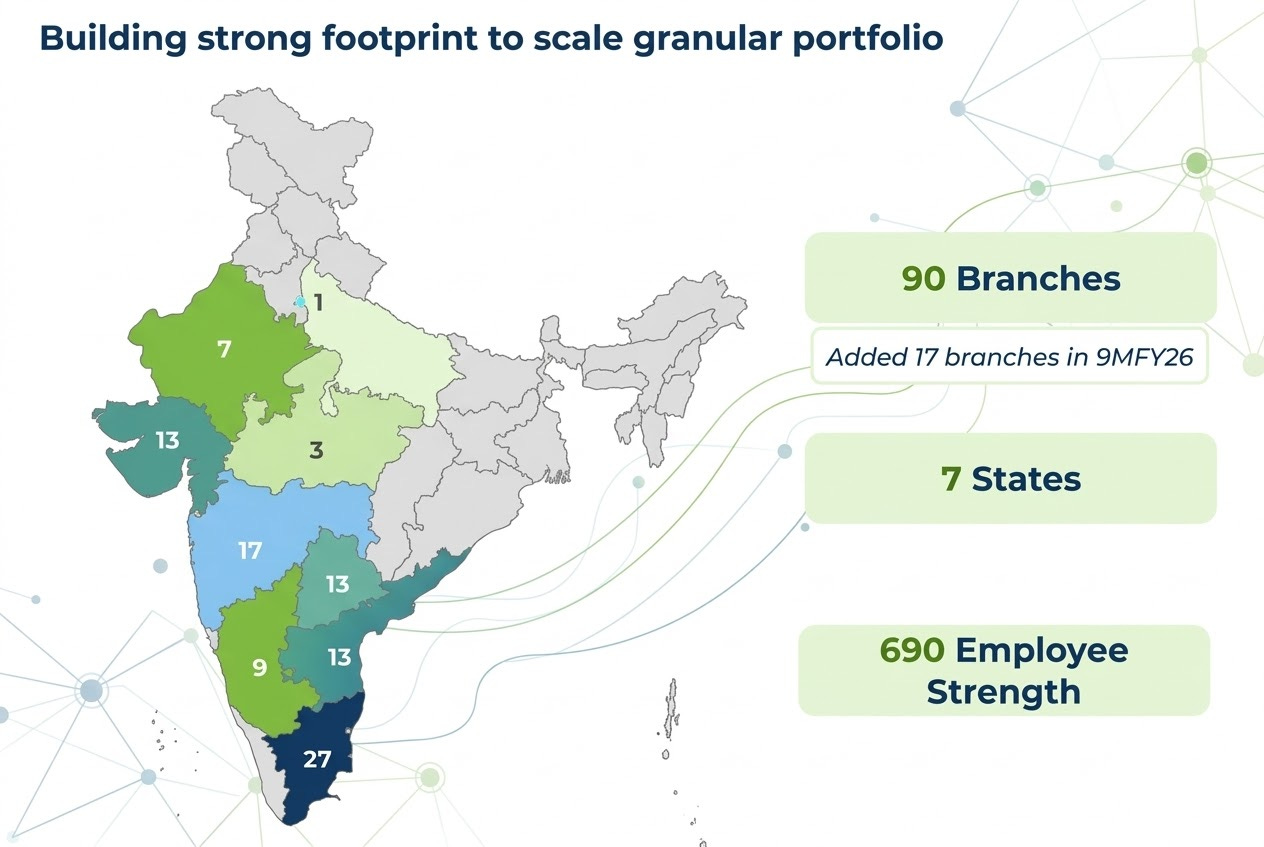

The Flagship Stores (Branch-led): Northern Arc operates its own physical branches (90 branches as of late 2025) across tier-2 to tier-6 cities. Here, they directly source larger, traditional MSME customers who require heavier evaluation and relationship-building.

The Pop-up Kiosks (Digital Partnerships): They also plug their digital lending APIs into the apps of over 50 Retail Lending Partners (Fintechs and payment gateways). When a merchant uses a partner’s app, Northern Arc is working behind the scenes to underwrite and disburse the loan instantly

b.) D2C Consumer Finance — The Digital Funnel

The consumer finance book is Northern Arc’s most technologically sophisticated segment and, as we will see later, its most epistemically demanding.

99% of originations are fully digital.

Loans come via 23+ fintech partners (EarlySalary, MoneyTap, LazyPay, KreditBee, etc.).

Ticket sizes: ₹50,000–₹5 lakh.

Tenors: 12–48 months.

Risk‑adjusted net yield: 15–16% (after partner share, FLDG, and credit cost).

About 70% of borrowers are repeat customers.

These borrowers are often salaried or self-employed individuals, including those from younger demographics, low-income backgrounds, or first-time, “new-to-credit” borrowers who lack a strong credit history. Their average bureau score is typically 650+

Because these loans are unsecured, credit cost is naturally higher: roughly 4.2–6% historically. To protect its own P&L, Northern Arc uses a strict First Loss Default Guarantee (FLDG) model:

The fintech partner is required to maintain a 5% FLDG deposit with Northern Arc. If a borrower defaults, the partner’s deposit absorbs the loss first, shielding Northern Arc’s core balance sheet.

In simple words: the partner that sourced the customer is the first one to bleed, which pushes them to keep quality high.

The High-Speed Operational Engine (nPOS and NuScore) To make money on small-ticket consumer loans, a lender must process massive volumes with minimal operational cost. Northern Arc achieves this using its proprietary technology stack:

nPOS: This is a cloud-based, API-enabled co-lending platform that plugs directly into the fintech partner’s app. It allows for seamless, straight-through processing of loans, including e-KYC, bureau checks, and disbursements.

NuScore: This is their in-house Machine Learning risk assessment algorithm. It instantly evaluates millions of data points and assesses actual borrower cash flows rather than relying solely on traditional bureau scores.

Together, these platforms allow Northern Arc to automatically underwrite and decision 20,000 to 25,000 loans in a single day with virtually zero manual intervention

c.) D2C Rural MFI — The Segment Northern Arc Deliberately Shrunk

Northern Arc addresses the deep rural market (where 90% of people lack formal credit access) through its dedicated, rugged subsidiary called Pragati Finserv.

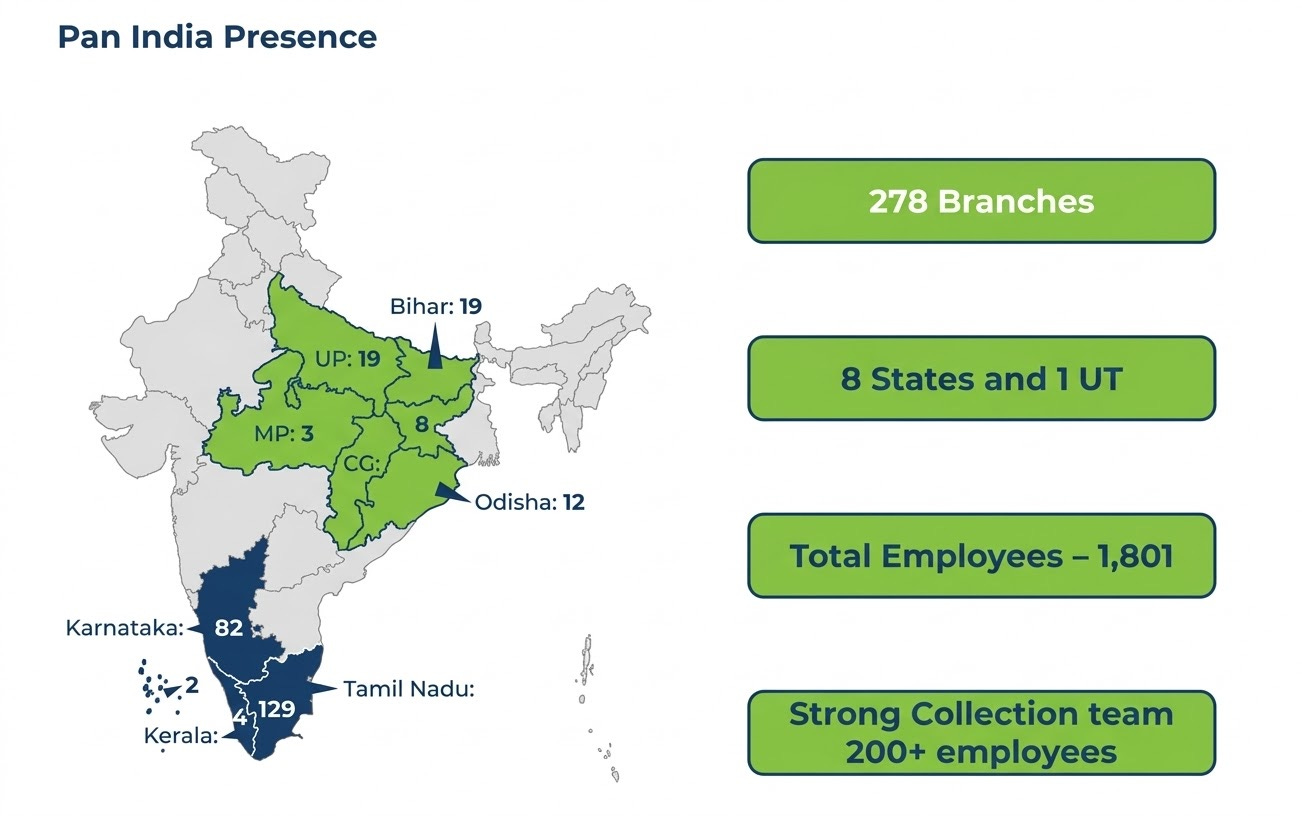

Unlike its digital consumer business, rural finance requires a heavy physical presence. Pragati acts as their “off-road vehicle,” operating a vast network of roughly 280 to 287 physical branches deep in the rural hinterlands.

They use a “Phygital” approach combining this intense physical, on-ground branch presence with digital workflows (like geo-tagging and digital KYC) to scale efficiently.

In FY25, Northern Arc made a decision that deserves significant credit. As MFI sector stress built over-leveraged borrowers, political headwinds, collections deteriorating across the sector, Northern Arc cut its rural/MFI exposure from a higher share to 6% of AUM.

Collection efficiency in Pragati was ~99.2% in FY24, but system-wide MFI over-leverage and some state-level noise (e.g., Karnataka ordinance) created a sector shock in FY24–25. With a ticket size of ₹50,000–₹75,000, coupon ~24.9%; group lending to low-income rural women.

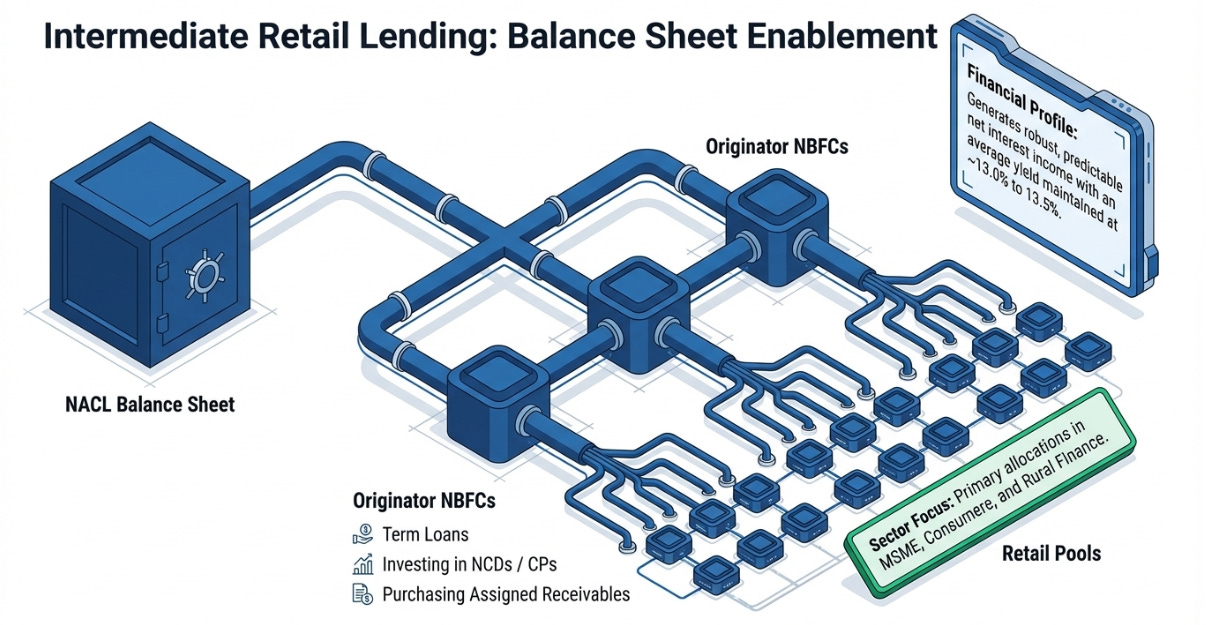

Engine 2 — Intermediate Retail Lending: Wholesale Capital for Retail Infrastructure

This is where Northern Arc looks least like a standard NBFC.

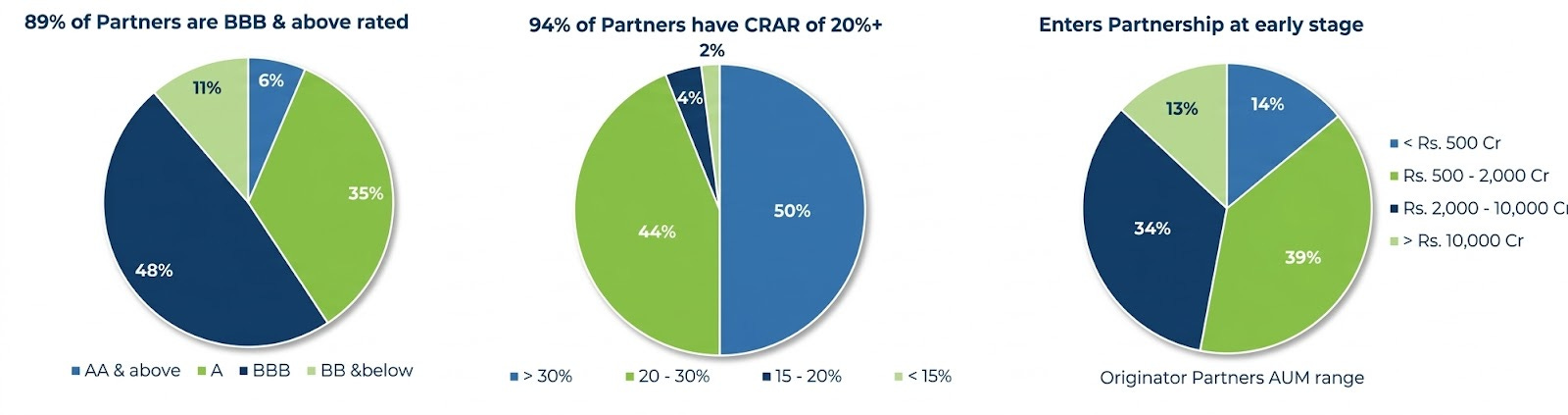

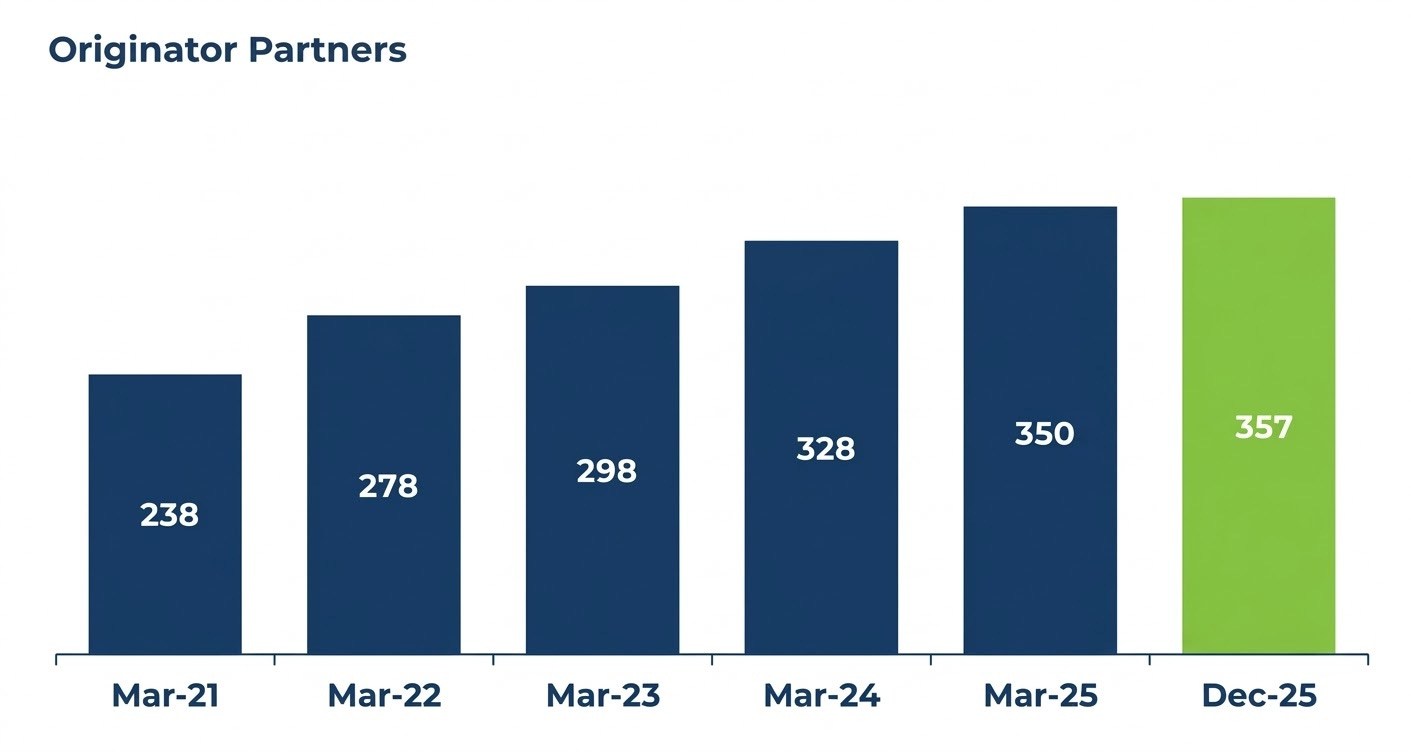

Intermediate Retail Lending (IRL) is lending to other lenders- the “originator partners”—rather than to the final borrower. As of Q3 FY26, this book stands at about ₹6,629 crore, roughly 44% of total AUM.

Borrowers: 350+ NBFCs, MFIs, HFCs, and fintech lenders across the country.

Product: term loans and working capital lines secured by their loan pools.

Economics: Northern Arc earns roughly a 3–3.5% spread over its own cost of funds.

Security: 110–120% pool cover—originators pledge loan assets worth 10–20% more than the amount borrowed.

Why does this exist alongside D2C?

IRL is how Northern Arc maintains its role as infrastructure even as it scales its own lending.

For a small MFI in Assam or a housing finance company in Gujarat, Northern Arc is often the only sophisticated institution willing and able to do this kind of underwriting. Without it, their funding cost might be 300–400 bps higher or unavailable entirely.

89% of IRL partners are rated BBB+ or above a deliberate quality gate.

Northern Arc’s edge here is not just its capital but its feedback loop:

It lends to originators.

It also structures and sells their loan pools onward to banks and funds.

It then sees how those pools actually perform over time under different structures and with different investors.

That full‑cycle view—origination to structuring to investor outcomes—is hard to replicate if you are “just a lender”.

Breakdown in Northern Arc’s world:

Local player (small MFI in Rajasthan, MSME lender in Tamil Nadu, vehicle financier in UP)

Sources customers using boots-on-ground: visits villages, knows who’s creditworthy via local intel

Creates loan pool (₹100-300 Cr of micro-loans at 18-25% yield)

Hands off to Northern Arc they clean/structure/sell to banks

Which creates flywheel: Originator access → Northern Arc structuring → bank funding → repayment data → better originators → bigger pools → repeat……

Originator = the “frontline lender” who finds and makes the actual loans to customers.

These partners operate close to the ground. They interact directly with underserved households and small businesses to figure out their credit needs. Many of them are relatively small in scale initially and have limited avenues to raise debt on their own.

Intermediate retail is the “shock absorber” line; it dilutes margin but stabilizes ROE when D2C is under stress. Northern Arc partners 350+ originators, each of which brings unique geo/data.

Aggregated: Predictable 3-4% PAR vs. solo 6-8%. Flywheel compounds as bad originators wash out, good ones scale.

Here is exactly how this works in the real world:

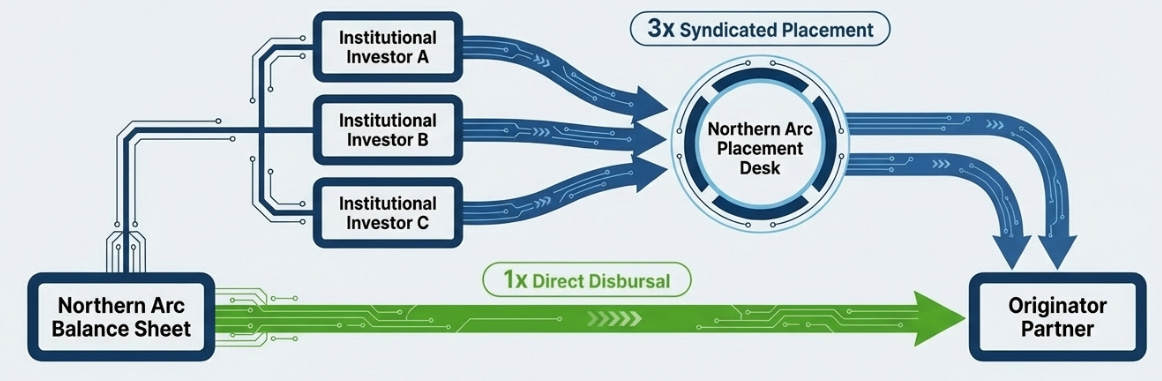

Engine 3 — Placements and Securitisation: The Throughput Business

Placements and securitisation is the purest “infrastructure” business inside Northern Arc.

Think of placements as toll revenue. Whenever capital moves from an institutional investor (a bank, mutual fund, insurer, DFI) to an originator’s loan pool via a structured deal that Northern Arc designs, Northern Arc collects a small fee - typically 20–25 basis points. The value lies in volume and repetition.

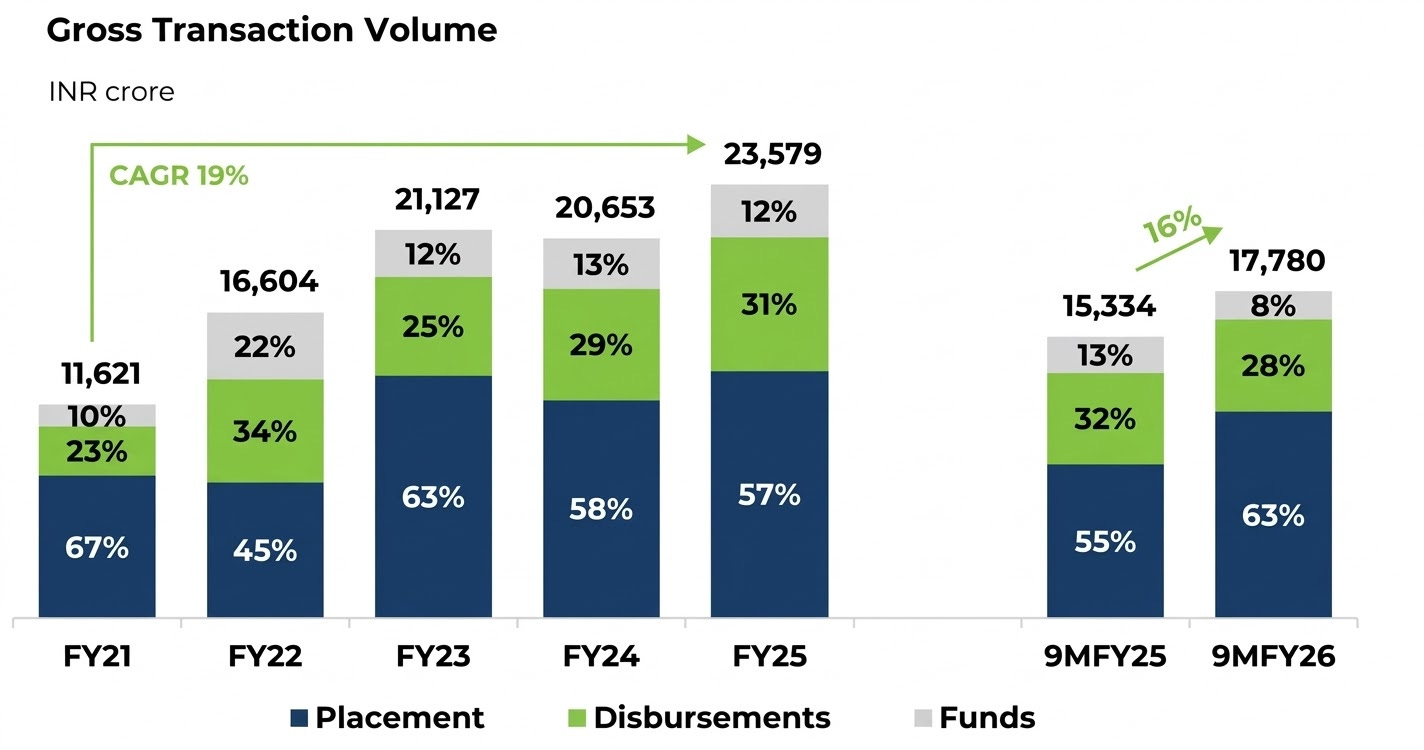

Cumulative placements facilitated since inception: about ₹1.14 lakh crore.

Q3 FY26 quarterly placements volume: ₹3,669 crore, up 73% year‑on‑year.

Mechanically, Northern Arc:

Aggregates and structures pools of loans from originators’ books.

Gets them rated.

Places them with institutional buyers (for example, banks looking to meet priority‑sector targets).

In Q3 FY26, placements volume hit ₹3,669 crore up 73% year-on-year. Over the life of the business, cumulative placements facilitated stand at ₹1.14 lakh crore. This is a staggering number. It means that across its existence, Northern Arc has moved over a hundred thousand crore rupees of credit risk from originators to institutional investors’ credit that would otherwise have sat inert in the system.

The fee is thin. But the economics are good because the capital intensity is minimal. Northern Arc does not hold these loans on its balance sheet. It structures, syndicates, and moves on. The P&L contribution is fee income with near-zero risk capital deployed. This is the infrastructure business at its purest.

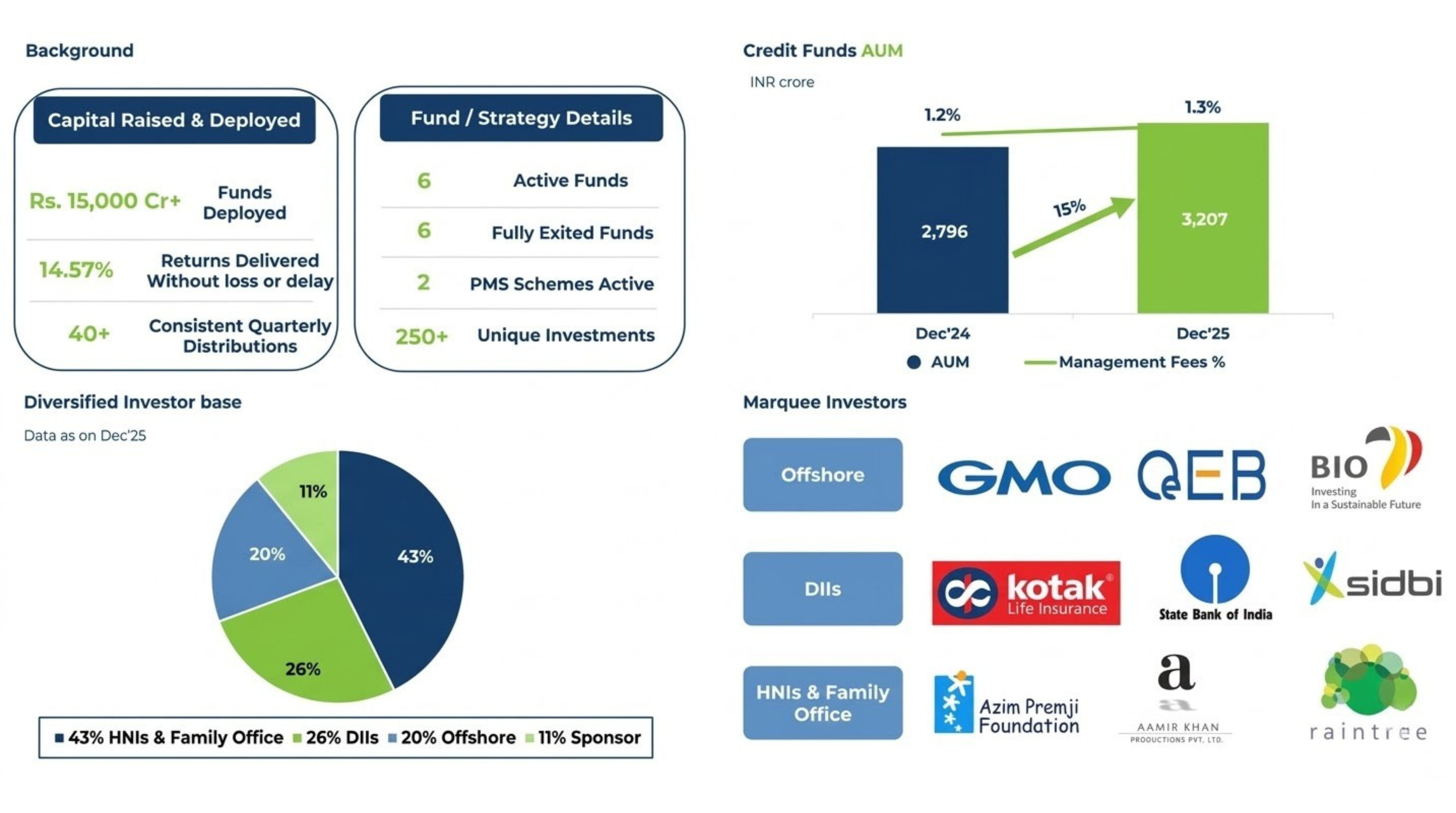

Engine 4 — NAIM: The In‑House Fund Manager

Northern Arc Asset Management (NAIM) manages ₹3,207 crore across 6 active credit funds. Another 6 funds have been fully wound down and exited all ahead of target returns. One fund targeted 13.5% IRR and delivered 14–17%. 1,200+ investors across institutional and semi-institutional categories.

NAIM earns approximately 110 basis points in management fees. More importantly, it provides a structural demand anchor for the placements engine — NAIM funds are steady institutional buyers of the securitisation structures that Northern Arc creates. The two businesses reinforce each other: the fund management operation creates a captive, sophisticated investor base for the credit infrastructure, and the credit infrastructure produces a consistent pipeline of yield-generating assets for the funds.

The Tech Stack: Real Edge or Good Marketing?

Northern Arc has four proprietary technology platforms: Nimbus, nPOS, NuScore, and Altifi. Management discusses them extensively. Investors cite them as moat. Sell-side research refers to the ‘tech DNA.’ This section will try to do something most coverage avoids: separate what is genuinely defensible from what is normal operational software dressed up as strategic infrastructure.

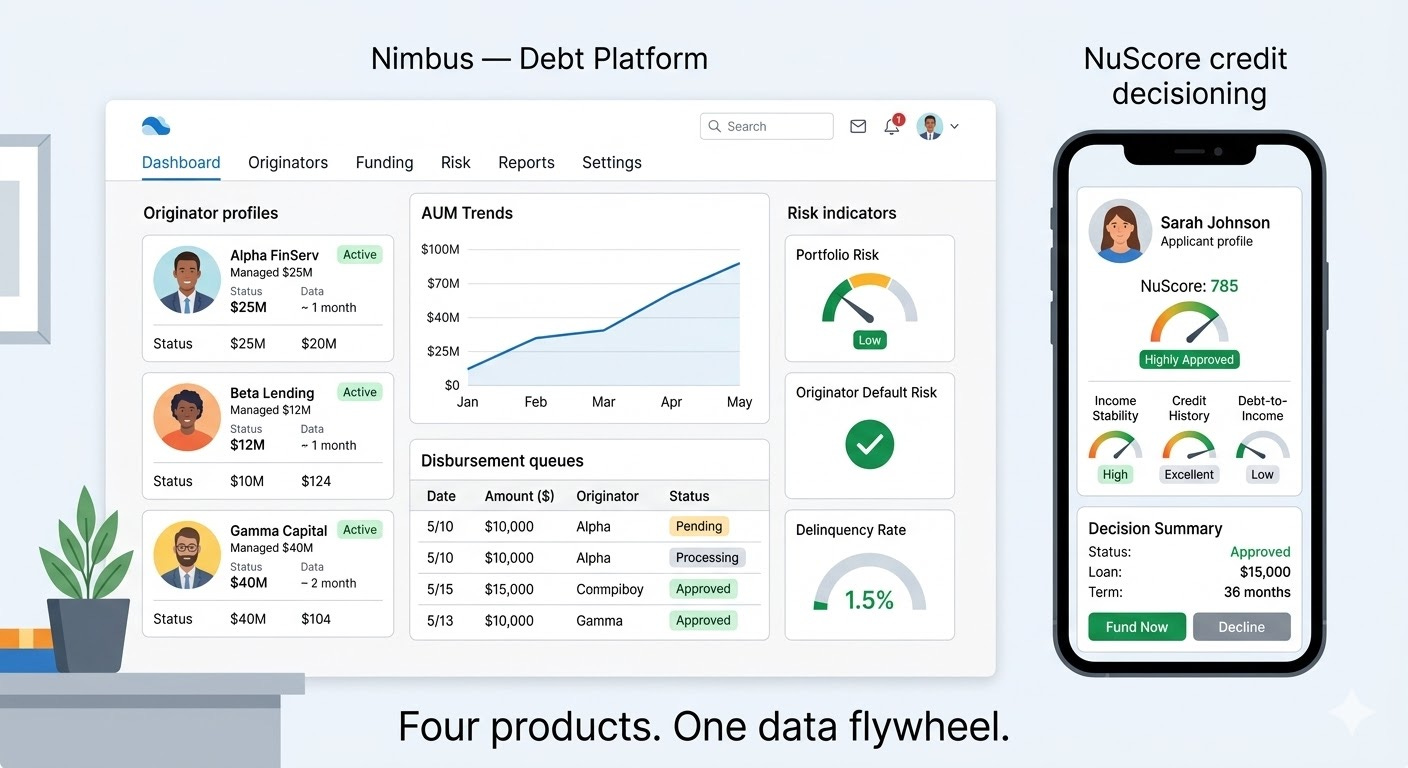

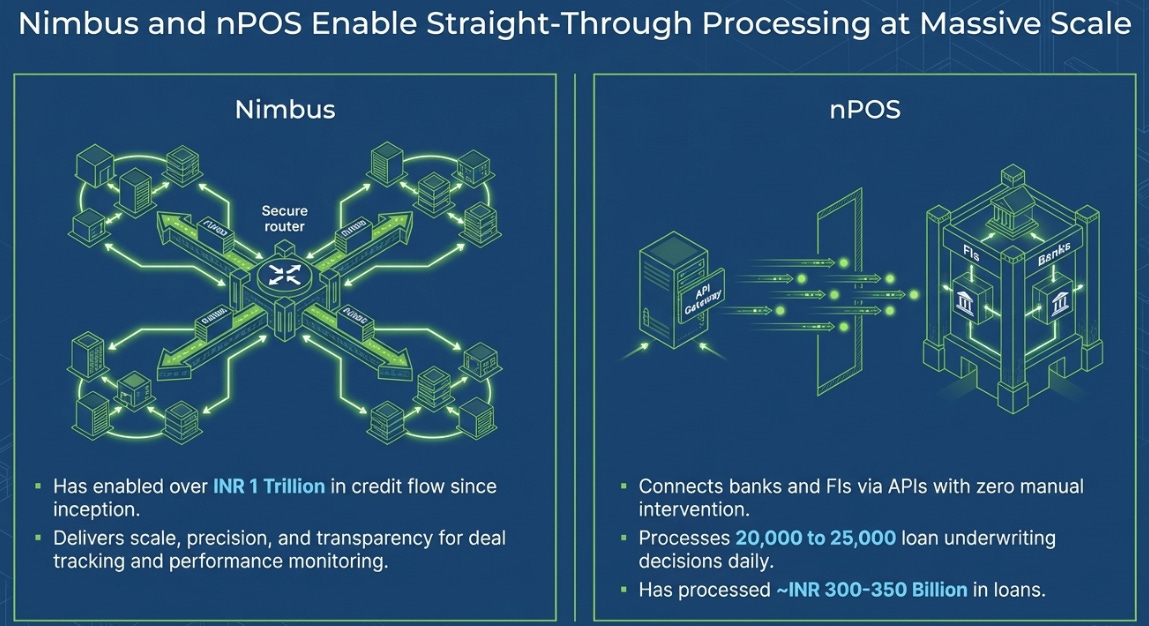

Nimbus — The Debt Origination Platform

Nimbus is Northern Arc’s institutional debt platform. It has processed ₹1 trillion+ in cumulative transactions and hosts 147 active originators. It is where deal origination, documentation, structuring, and monitoring happen.

What it genuinely does: reduces operational friction for institutional investors doing credit. Standardizes deal documentation. Creates audit trails that make due diligence faster for repeat investors. In a market where deal execution often involves weeks of back-and-forth legal documentation, Nimbus compresses this.

What it isn’t: a moat. Any sufficiently-funded competitor can replicate this. CredAvenue (now Yubi) has built a similar institutional debt marketplace. The tech itself is not proprietary. The moat, if any, is switching costs once a mutual fund’s credit desk has its templates built around Nimbus deal formats and its compliance team has built approvals around Nimbus documentation, switching to a competitor requires reconfiguring institutional workflows. That switching cost is real but modest.

nPOS — The Co-Lending Operating System

nPOS is the API platform that enables co‑lending with banks and fintechs.

Handles 20,000–25,000 credit decisions per day.

Has processed over ₹10,000 crore of co‑lending volume in FY25

It allows Northern Arc and bank partners to jointly underwrite and disburse loans in near-real-time.

The genuine value here is operational plumbing. Co-lending is regulatory mandated for certain categories, but operationally complex, as two institutions need to share information, reconcile decisioning, split disbursements, and track repayments jointly. nPOS handles this machinery. It is a valuable operational infrastructure.

But again, it is replicable. The value is in the client relationships and the trained bank teams on both sides, not in the API architecture itself.

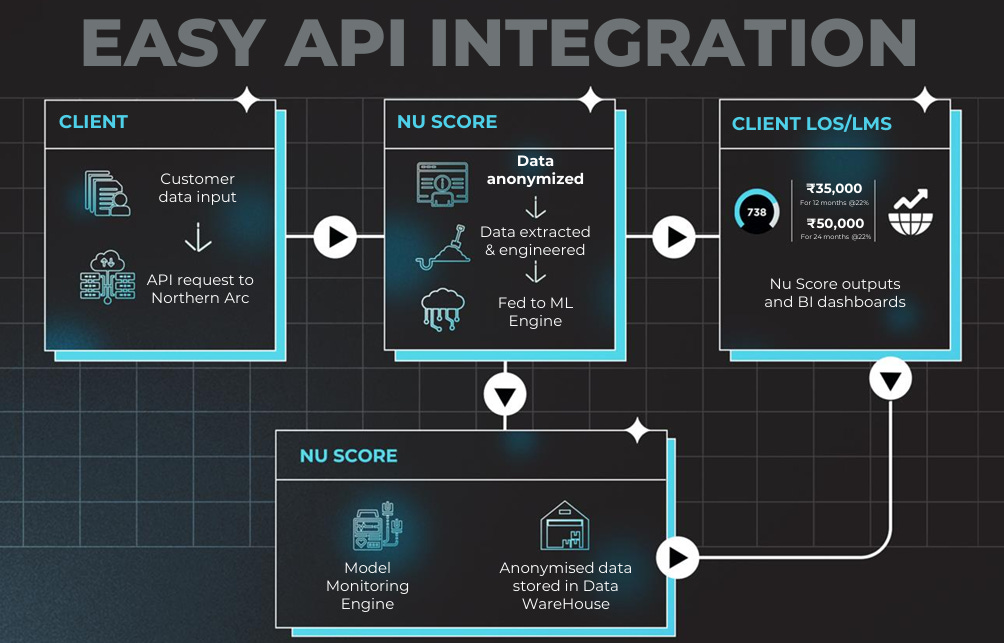

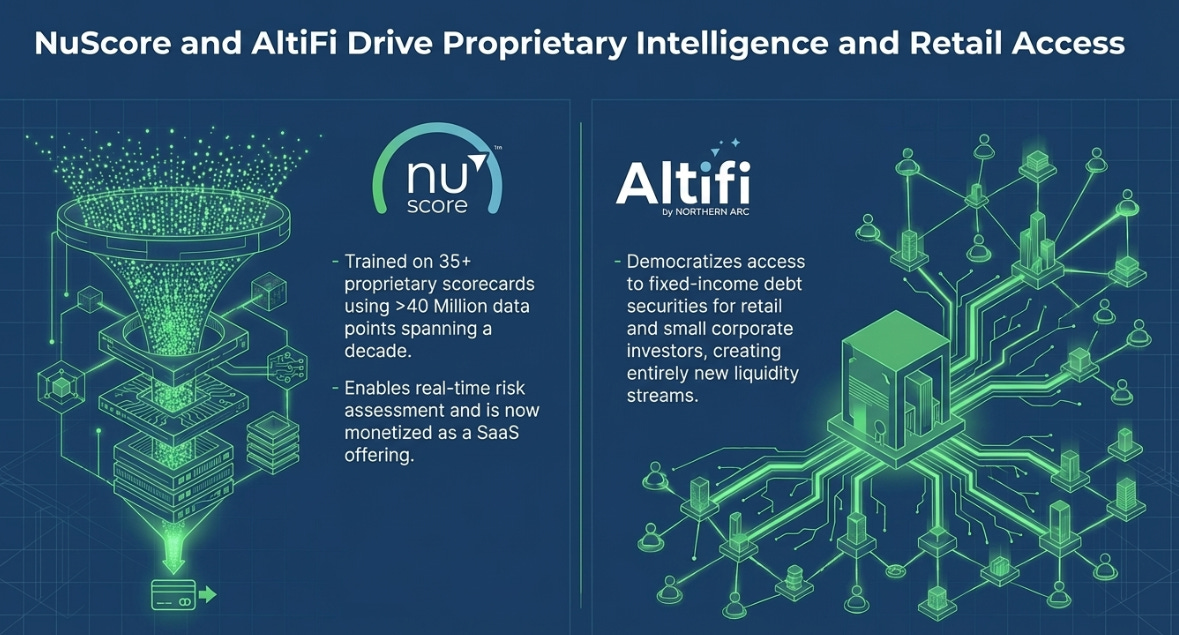

NuScore — The Underwriting Engine

NuScore is genuinely the most interesting technology asset in the business and also the one that requires the most scrutiny.

It is a machine‑learning underwriting model trained on 40+ million data points.

It includes 15 years of credit history, spanning IL&FS, COVID, and the recent MFI stress cycle.

It powers digital consumer underwriting and is being sold as SaaS to other lenders.

Models trained on data of this vintage and diversity are rare in Indian credit. The ability to segment risk in sub-prime and near-prime cohorts with this level of historical depth represents a meaningful informational edge in theory.

The honest limitation: Northern Arc recorded a one‑time Expected Credit Loss (ECL) adjustment of ₹23.4 crore on older consumer digital cohorts structured with FLDG. That was effectively an admission that NuScore had been too optimistic about forward losses for years in that book. Actual credit outcomes were worse than the model predicted, and provisions had to be topped up.

THE HARD QUESTION

If NuScore’s feedback loop is as fast and accurate as claimed, ‘brutally reactive’ to early delinquency signals, how did a multi-year systematic underestimation accumulate in the consumer digital book without triggering model recalibration? Either the feedback loop works slower than marketed, or the FLDG accounting structure introduced a lag that obscured the signal. Both answers have implications for the credit thesis.

This is not a reason to dismiss NuScore’s value. It is a reason to be precise about what it does and doesn’t do. NuScore is a genuinely useful underwriting tool that improves credit selection in Northern Arc’s origination channels (which is the best in class, even banks refer to their risk assessment as the industry standards). The SaaS monetization is an interesting option value, but the core claim that Northern Arc’s data advantage creates compounding credit superiority requires more evidence than management assertions.

Altifi — The Option Nobody Is Pricing

Altifi is Northern Arc’s retail bond platform. 45,000+ registered users. ₹303 crore in transactions in FY25. It offers retail investors access to fixed-income instruments bonds, debentures, structured products backed by Northern Arc’s originator network.

Coverage gives these two sentences. That is a mistake.

Altifi’s strategic significance is not what it has already achieved ₹303 crore is immaterial to a ₹15,000 crore AUM business. The significance is what it could become. If Altifi scales, it creates a two-sided marketplace: originator credit pools seeking distribution on one side, retail debt investors seeking yield on the other, with Northern Arc as the trusted curator and underwriter in the middle.

This is a structurally different business from a balance-sheet lender. If successful, Altifi makes Northern Arc look less like an NBFC and more like an operating system for India’s retail fixed-income market. That warrants a meaningfully higher multiple than a 1.1x book value lender.

Altifi is the largest unpriced optionality in the Northern Arc story. It is also the most execution-dependent. Retail investor education in Indian fixed income is a decade-long project, not a product launch. We have seen this trend playout in developed countries, as they mature investors move to debt fund and fixed income sources.

Management Mindset: This is not a separate SaaS company yet; it’s an internal nervous system that does three things:

Lowers operating cost per loan and per placement.

Sharpen risk-adjusted pricing through granular, real-time feedback.

Creates optionality to sell tech/services to third parties, adding high-margin, low-capital fee lines over time.

The D2C Identity Crisis

Northern Arc’s most under‑discussed issue is not credit quality or technology. It is identity.

The D2C pivot began as a logical response to a margin problem. As a pure wholesale/infrastructure lender, Northern Arc’s spreads on Intermediate Retail Lending are 3–3.5%. Reasonable, but thin. If you can lend directly to MSMEs and consumers instead, and earn 17–20% on LAP and 15–16% net on consumer digital, the NIM improvement is immediate and substantial.

The logic is clean. The second-order effects are not.

The Conflict of Interest — Never Compete with Your Customer

Northern Arc’s entire institutional positioning rests on being a neutral infrastructure layer. Its 350+ originator partners use Northern Arc for funding, structuring, distribution, and advisory. They trust Northern Arc because Northern Arc is not competing with them for the same borrower.

That assumption is now structurally compromised.

When Northern Arc originates MSME LAP in Tamil Nadu , it is deploying balance sheet capital into the same segments, geographies, and borrower profiles that its originator partners serve. The MFI lender who depends on Northern Arc’s IRL funding and securitization services is now watching Northern Arc go direct into adjacent segments. The fintech originator whose loan pool Northern Arc structures and distributes to institutions is now observing Northern Arc deploy its own capital into similar cohorts.

So?

Imagine you run a specialized port facility. Shipping companies bring their cargo to you for processing, documentation, and distribution. You are the neutral infrastructure. Now imagine you start running your own shipping company using the same port and competing with the same cargo owners on the same routes. The shipping companies don’t suddenly lose access to the port. But the relationship changes. The neutral party has become a competitor in a role where trust was the product.

The management's answer to this challenge is geography and segment differentiation. Northern Arc claims to be targeting different ticket sizes and geographies than its originator partners. This is a partial answer. It may hold for now. As the D2C book scales toward ₹15,000–20,000 crore over the next three years, the differentiation becomes harder to maintain.

Which Version of Northern Arc Is the Market Pricing?

This is where the strategic identity question becomes a valuation question.

If Northern Arc is primarily an infrastructure and fee-income business using its balance sheet selectively to support the platform, not as the primary growth driver the right term to use is CRISIL or CAMS or CDSL: asset-light, moat-protected, fee-compounding businesses that deserve premium multiples.

If Northern Arc is primarily a D2C NBFC that happens to have a structuring arm and a fund management sidecar, the right player is Five-Star Business Finance or SBFC or Arman Financial. Excellent lenders with good credit processes trades at 2–3x book on a good cycle.

Valuation: What Is This Actually Worth?

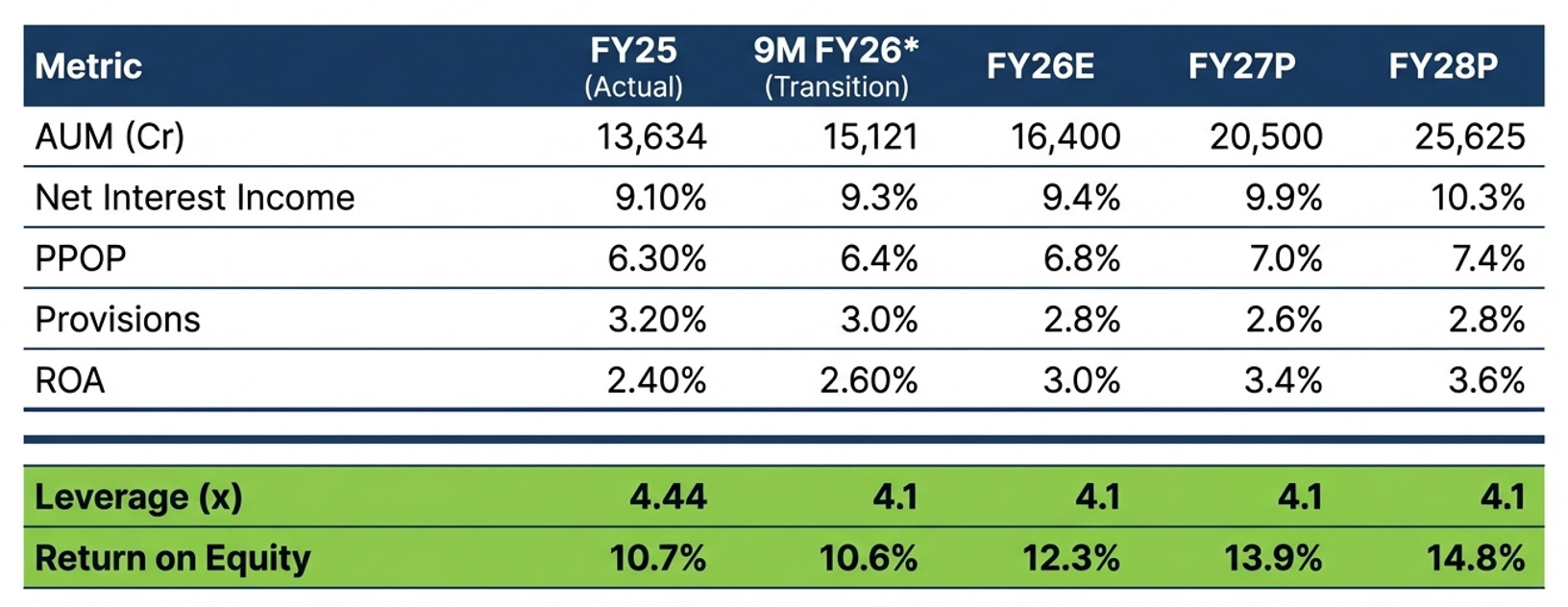

The economics of lending businesses eventually reduce to a simple equation: return on assets, multiplied by leverage, determines return on equity.

If you have come this far than you might have understood how the underlying economics are changing. Return on assets is expected to expand from roughly 2.4% to around 3.6% over the next 2 years, all thanks to better spreads, operating leverage and improving credit costs. Importantly, this improvement is not coming from higher leverage. In fact, leverage remains relatively stable.

This means the expansion in return on equity from roughly 10–11% today to nearly 15% in the outer years is being driven primarily by operational improvements rather than taking head on balance-sheet risk.

In the world of NBFCs, valuations tend to follow a fairly simple logic. Businesses that consistently generate low-teen returns on equity typically command modest price-to-book multiples, while those that can sustainably deliver mid-to-high teens returns are rewarded with significantly higher valuations.

Where Northern Arc ultimately sits on this spectrum will depend on how the market interprets its business model.

If it is viewed purely as another lending NBFC, its valuation will likely track the conventional relationship between ROE, growth and credit risk. But if investors begin to see the company as something slightly different a layer of infrastructure that connects fragmented credit demand with institutional capital, then the business may deserve to be evaluated through a different lens.

What Justifies the Multiple?

The central multiple question is whether Northern Arc deserves to trade closer to a wholesale NBFC (1x book) or a well-run NBFC with good underwriting DNA (3–4x book). The answer depends entirely on which version of the business proves dominant over the next five years.

The bear case (current price at lower end): D2C competition intensifies in MSME LAP. Originator trust erodes as D2C scales. Credit costs stay elevated as MFI stress takes longer to resolve. NuScore recalibration reveals additional legacy digital cohort issues. ROA stalls at 2.2–2.5%. At 1x book, the stock barely moves from current levels. This is the ‘nothing went wrong, but nothing went right’ scenario.

The base case (approximately 2x FY28 book): Credit costs normalize to 2.5–3.0% or below by FY27. D2C grows to 75% of total AUM without materially impairing IRL. NuScore SaaS gains three to four anchor clients. ROA expands to 3.4–3.6% and P/B inches towards 2.0x or higher.

The bull case (Well-run NBFC): By FY28, Altifi has 3–5 lakh retail investors and ₹5,000 crore in transactions. NuScore SaaS has 10+ paying clients. The fee income contribution crosses 45% of PBT, which further materially improves ROA. The market begins pricing Northern Arc as a sustainable, and higher NIM lender rather than an Wholesale NBFC (with 3-4% NIM). P/B re-rates to 3.0x or higher.

Where Does Real Value Capture Happen?

This is the essential investor question. For Northern Arc, value accrues in precisely four places:

First, in the spread between portfolio yield (16.9%) and cost of funds (8.5–9.0%), generating the ~8% NIM that funds the credit cost and operating expenses with room for profit. This is the stable engine.

Second, in the placements fee machine capital-efficient, growing at 70%+ annually, and directly correlated with institutional credit market depth. This is the upside accelerant.

Third, in the data and underwriting intelligence 40M+ data points, 15 years of through-cycle calibration that allows Northern Arc to price risk better than most competitors. This is the edge that is hardest to replicate quickly.

Fourth and this is the option, not the base case, in Altifi. If retail distribution of fixed income products via Altifi scales, Northern Arc stops being priced as a pure play lender and starts being priced as an integrator. The entire business re-rates.

The Questions to Track

These are the specific datapoints that will tell you, quarter by quarter, whether the thesis is tracking or breaking:

IRL book growth (₹ crore QoQ). If this stagnates or shrinks as D2C grows, originator trust is being impaired. This is the single most important leading indicator for the business.

Non-interest income as % of PBT. The journey from 36% to 45%+ is the signal that ROA will be more sustainable. If these metric reverses, reassess.

Altifi transaction volume. Any quarter where this number grows faster than 100% YoY is a signal the retail distribution option is real. Watch for institutional investor onboarding to the platform.

Track how they are performing and other key KPIs in new segments like Vehicle financing, Affordable Housing Finance and Agri Finance.

GNPA and Credit cost trajectory in the consumer digital book. The FLDG adjustment in FY25 cleaned up old cohorts. The question is whether FY23 and FY24 origination vintages underwritten under the recalibrated NuScore perform better. First data should be visible in FY26 results.

Final Thought — THE INFINITY WAR

There is an old rule in Indian financial services. Capital is abundant. Trust is scarce. Every institution that has tried to bridge India’s ₹trillion credit gap has eventually hit the same wall: not a shortage of money, not a shortage of borrowers, but the near-impossibility of making capital trust risk it cannot see.

Northern Arc’s first fifteen years were spent solving exactly that problem. Building the telemetry. Earning the institutional credibility. Surviving the shocks that destroyed peers. Using each crisis as a laboratory.

The model is now built. The refinery is running.

The harder questions are what come next. Whether the moat is actually defensible when Vivriti runs the same playbook. Whether the D2C pivot is a disciplined extension of the platform or the beginning of a slow drift toward the warehouse model Northern Arc was designed to replace. Whether the P&L with its unusual two-floor structure of spread income and platform fees justifies a valuation premium, or whether the market’s skepticism is correctly priced.

And ultimately: what you are actually paying for when you buy this stock, and what has to be true for that price to be right.

In Part 2, we take the model apart under stress the competitive arena, the liability stack, the three credit theatres where the real risk lives, and what is driving these valuation frameworks.

To be continued.……

Stay tuned, see you next time!

Until then… Share your views in the comments!

Disclaimer: This article is provided for informational purposes only and should not be considered as investment advice

P.S.: Abhay, Manthan/Writer- No Buy/Sell Recommendation!

Very thorough and in-depth article. Not everyone can write such an insightful analysis of this multi-faceted entity. Kudos to Manthan, Abhay and Alpha Ventures.

Brilliant article. Eagerly waiting for part 2